Dr. Laurence Kotlikoff believes that the total U.S. national dept and obligations of $200 trillion puts the country in worse financial condition then Russia or China.

Are you bombarded by daily reports of the stock market hitting record highs, and the Fed promising to stop propping up stocks, real estate, and bonds? Ever wonder if now is finally the time to throw caution to the wind, get off the sidelines, and jump onto the profit wave to reap some those tempting and seemingly unstoppable gains you may have been missing out on?

Or maybe you sense it’s almost the end of the party, and are concerned that the skyrocketing debt and teetering banks mean it’s really time to not be the last one to the exits!

Russian deputy foreign minister Igor Morgulov said on Monday that "an apocalyptic scenario of developments" on the Korean Peninsula is possible, but Russia hopes that a common sense would prevail among the involved parties.

"A scenario of the apocalyptic development of the situation on the Korean Peninsula exists and we cannot turn our blind eye to it," Morgulov said speaking at the opening of the eighth annual Asian Conference of the Valdai discussion club in Seoul. "I hope that a common sense, pragmatism and an instinct of self-preservation would prevail among our partners to exclude such negative scenario," the Russian diplomat said, quoted by Russia's Tass.

Fire and brimstone aside, Morgulov noted that a phase of calm appeared to be returning as North Korea’s current pause in provocations - the longest since last winter - indicates a step toward denuclearization of the Korean peninsula. “I think North Korea’s restraint for the past two months is within the simultaneous freeze road map” suggested by China and Russia, Morgulov told reporters in Seoul on Monday according to Bloomberg. North Korea’s last provocation was on Sept. 15, when it fired its second missile over Japan in as many months. The 73-day pause is the longest since a 116-day break between October 2016 and February.

Russian and Chinese foreign ministers proposed in July a “double freezing” initiative, under which North Korea refrains from missile and nuclear tests, and the U.S. and South Korea halt large-scale military exercises, however the U.S. has rejected this proposal, arguing that its drills are defensive in nature. Earlier this month, it carried out its first exercise in a decade using three aircraft carriers in the region, and plans to conduct drills with South Korea’s air force in early December.

Morgulov, Russia’s deputy minister responsible for relations with East and South Asia, said that following a “freeze for freeze” the next step would be to hold exchanges with Pyongyang. Once North Korea agrees to a moratorium on testing and talks are taking place, the process can move to discussion of denuclearization, he said. “We will have to see a certain change of attitude of the U.S., especially on freezing or reducing” its military drills, Morgulov said. “It’ll be difficult for us to play the role of persuading North Korea” not to provoke anymore without a change in the U.S. position.

Despite the impasse, and underscoring Russia's argument, the diplomat said that "we have told North Korea many times that for us [its] nuclear status is unacceptable," adding that "we continue this work with the North Korean counterparts presenting to them our position."

Moscow negatively assess joint military drills of the United States with its allies in the region of the Korean Peninsula, while North Korea keeps a two-month pause in missile and nuclear tests, he went on.

"Considering the two-month long period of silence, the United States is not planning to reduce the scale of its regular military exercises, but also plan holding sudden drills as well," Morgulov said. "Unfortunately, this is the answer, which North Korea gets in response to its two-month silence," the Russian diplomat said adding that Moscow "assesses it negatively." "I believe that both the North Korean nuclear tests and joint military drills of the United States with its allies are definitely of a negative nature," Morgulov said.

"Russia has presented the roadmap’s contents both to the U.S. and to the DPRK," the diplomat said. "I would like to say that "at the very entrance" the plan has not been rejected either by Washington or by Pyongyang, though still no answer."

"Besides, we have spoken for discussing certain elements of this plan separately with the U.S. and with North Korea," he continued. "We have begun the work, but I have to say regretfully that the actions, which Washington undertook in October-November, I mean the unplanned drills, affect greatly our dialogue on settlement on the basis of the roadmap."

"Is it possible for someone to cherish illusions that threats from US President Donald Trump to strike with ‘fire and fury’ will be able to cut the knot, which has been tight on the Korean Peninsula for many decades?" Morgulov said. "I believe it would be naive to hope that any of the sides would give in to the pressure," the Russian diplomat said.

"We must understand that the pressure borders with the deliberate push of North Korea to the humanitarian catastrophe," Morgulov said. "This will not result in the North Korean authorities giving up missile and nuclear programs, but on the contrary, will only strengthen its intentions to stay until the very end."

"I believe that the path of pressure has no perspectives and there is no other alternative to the dialogue," the Russian diplomat said.

"The resumption of inter-Korean dialogue could have a positive effect (on the conflict settlement)," Morgulov said. "These two countries have issues to discuss and I know that our South Korean partners are ready for such dialogue and repeatedly expressed interest in its initiation," the Russian diplomat said.

"If Pyeongyang’s demonstrated restraint over the past two months was met with similar reciprocal steps on behalf of the United States and its allies then we could have moved to the start of direct talks between the United States and North Korea," Morgulov said.

"Will it be possible? I am absolutely sure that it is possible," the Russian diplomat said. "The key agenda of such talks can be very simple, which is the principles of peaceful coexistence. I believe that the lack of such concord gives roots to hostility and mutual mistrust among the involved parties."

"The United States and its allies should at least reduce the scale of their regular military exercises they are holding in the region of the Korean Peninsula," Morgulov said.

Gold and silver expert Rob Kirby says the price suppression of gold and silver is in the process of ending. Kirby says, “In the very near future... we are going to experience precious metals to be cryptoized and put on the blockchain. These are going to be superior alternatives to GLD and SLV, and this will bring transparency to the price discovery process for both gold and silver.

What this means is GLD, SLV and COMEX are going to be made irrelevant by the cryptoizing of physical metal.” Kirby predicts, at some point, the price of physical gold and silver will skyrocket, and the same bankers who suppressed the price will turn around and send it to the moon. Kirby contends, “When the banks feel this is a foregone conclusion, that the price of gold and silver are going up, they are going to try to front run it. Banks try to front run everything.”

When capital is mentioned in the present-day political debate, the term is usually subject to a rather one-dimensional interpretation: Whether capital saved by citizens, the question of capital reserves held by pension funds, the start-up capital of young entrepreneurs or capital gains taxes on investments are discussed – in all these cases capital is equivalent to “money.” Yet capital is distinct from money, it is a largely irreversible, definite structure, composed of heterogeneous elements which can be (loosely) described as goods, knowledge, context, human beings, talents and experience. Money is “only” the simplifying aid that enables us to record the incredibly complex heterogeneous capital structure in a uniform manner. It serves as a basis for assessing the value of these diverse forms of capital.

Modern economics textbooks usually refer to capital with the letter “C”. This conceptual approach blurs the important fact that capital is not merely a single magnitude, an economic variable representing a magically self-replicating homogenous blob but a heterogeneous structure. Among the various economic schools of thought it is first and foremost the Austrian School of Economics, which stresses the heterogeneity of capital. Furthermore, Austrians have correctly recognized, that capital does not automatically grow or perpetuate itself. Capital must be actively created and maintained, through production, saving, and sensible investment.

Moreover, Austrians emphasize that one has to differentiate between two types of goods in the production process: consumer goods and capital goods. Consumer goods are used in immediate consumption – such as food. Consumer goods are a means to achieve an end directly. Thus, food helps to directly achieve the end of satisfying the basic need for nutrition. Capital goods differ from consumer goods in that they are way-stations toward the production of consumer goods which can be used to achieve ultimate ends. Capital goods therefore are means to achieve ends indirectly. A commercial oven (used for commercial purposes) is a capital good, which enables the baker to produce bread for consumers.

Through capital formation, one creates the potential means to boost productivity. The logical precondition for this is that the production of consumer goods must be temporarily decreased or even stopped, as scarce resources are redeployed toward the production of capital goods. If current production processes generate only fewer or no consumer goods, it follows that consumption will have to be reduced by the quantity of consumer goods no longer produced. Every deepening of the production structure therefore involves taking detours.

Capital formation is therefore always an attempt to generate larger returns in the long term by adopting more roundabout methods of production. Such higher returns are by no means guaranteed though, as the roundabout methods chosen may turn out to be misguided. In the best case only those roundabout methods will ultimately be continued, which do result in greater productivity. It is therefore fair to assume that a more capital-intensive production structure will generate more output than a less capital-intensive one. The more prosperous an economic region, the more capital-intensive its production structure is. The fact that the generations currently living in our society are able to enjoy such a high standard of living is the result of decades or even centuries of both cultural and economic capital accumulation by our forebears.

Once a stock of capital has been accumulated, it is not destined to be eternal. Capital is thoroughly transitory, it wears out, it is used up in the production process, or becomes entirely obsolete. Existing capital requires regularly recurring reinvestment, which can usually be funded directly out of the return capital generates. If reinvestment is neglected because the entire output or more is consumed, the result is capital consumption.

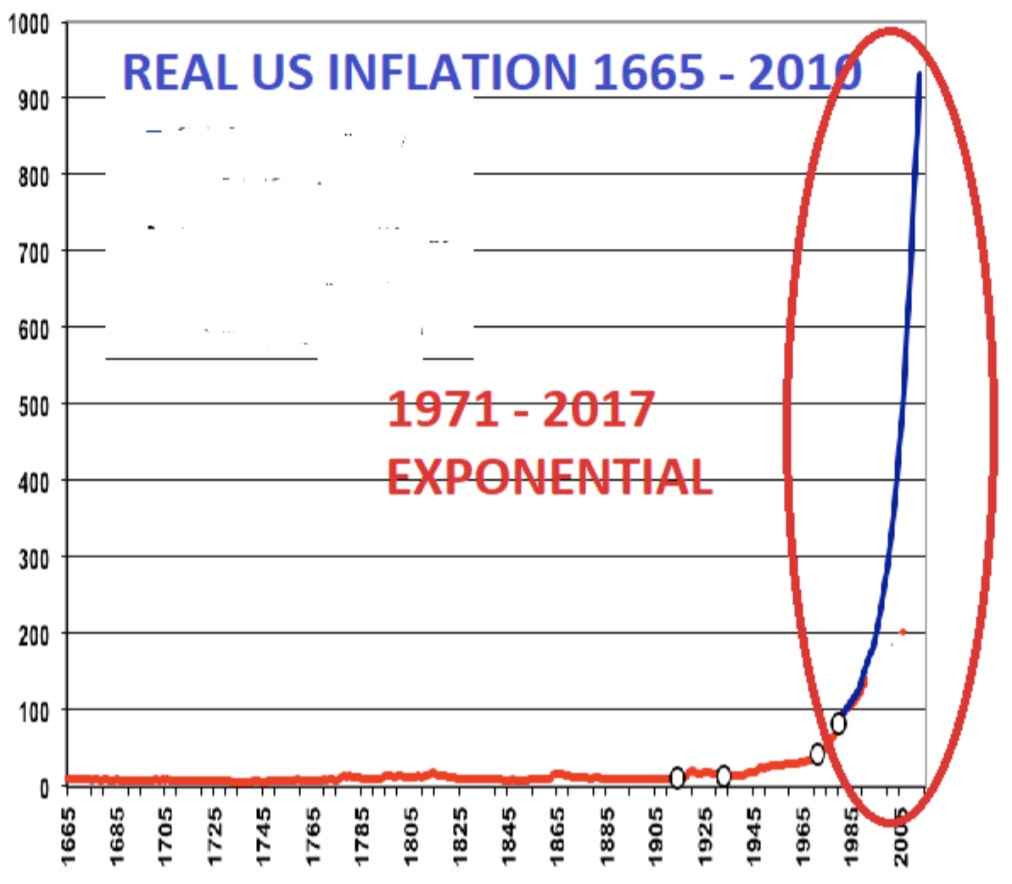

It is not only the dwindling understanding of the nature of capital that leads us to consume it without being aware of it. It is also the framework of the real economy which unwittingly drives us to do so. In 1971 money was finally cut loose entirely from the gold anchor and we entered the “paper money era.” In retrospect, it has to be stated that cutting the last tie to gold was a fatal mistake. Among other things, it has triggered unprecedented instability in interest rates. While interest rates displayed relatively little volatility as long as money was still tied to gold, they surged dramatically after 1971, reaching a peak of approximately 16 percent in 1981 (10-year treasury yield), before beginning a nosedive that continues until today. This massive decline in interest rates over the past 35 years has gradually eroded the capital stock.

An immediately obvious effect is the decline in so-called “yield purchasing power”. The concept describes what the income from savings, or more precisely the interest return on savings, will purchase in terms of goods. The opportunity to generate interest income from savings has of course decreased quite drastically. Once zero or even negative interest rate territory is reached, the return on saved capital is obviously no longer large enough to enable one to live from it, let alone finance a reasonable standard of living. Consequently, saved capital has to be consumed in order to secure one's survival. Capital consumption is glaringly obvious in this case.

It is beyond question that massive capital consumption is taking place nowadays, yet not all people are affected by it to the same extent. On the one hand, the policy of artificially reducing the interest as orchestrated by the central banks does negatively influence the entrepreneurs’ tasks. Investments, especially capital-intensive investments seem to be more profitable as compared to a realistic, i. e. non-interventionist level, profits are thus higher and reserves lower. These and other inflation-induced errors promote capital consumption.

On the other hand, counteracting capital consumption are technological progress and the rapid expansion of our areas of economic activity into Eastern Europe and Asia in recent decades, due to the collapse of communism and the fact that many countries belatedly caught up with the monetary and industrial revolution in its wake. Without this catching-up process it would have been necessary to restrict consumption in Western countries a long time ago already.

At the same time, the all-encompassing redistributive welfare state, which either directly through taxes or indirectly through the monetary system continually shifts and reallocates large amounts of capital, manages to paper over the effects of capital consumption to some extent. It remains to be seen how much longer this can continue. Once the stock of capital is depleted, the awakening will be rude. We are certain, that gold is an essential part of any portfolio in this stage of the economic cycle.

Since President Recep Tayyip Erdogan installed himself as ‘Sultan for life’, the Turks appear to have had a dramatic change of heart towards the barbarous relic…

The Turks have never imported a greater value of gold than in the last 12 months…

Addditionally, as Bloomberg reports, Bar and coin purchases, a measure of investment demand, were 47 metric tons so far in 2017, compared with 14.8 tons in the same period a year ago, according to a report from the World Gold Council published Thursday.

The weak lira and “President Erdogan’s pro-gold comments in November last year continued to lend support to the market,” the gold council said.

But it’s not just the average Turk who is buying gold, Turkey’s central bank is also buying gold, increasing purchases by 30.4 tons during the third quarter.

While the central bank has cited a good old-fashioned diversification policy, some analysts speculated that the country could be shoring up reserves amid rising tensions between Turkey and its traditional Western allies.

A year ago, President Recep Tayyip Erdogan urged Turks to prefer gold to the U.S. dollar as a savings vehicle, and asked the central bank to support that policy.

And gold is doing exactly what it should do as faith in fiat falters.

The question is – just like in India – how long before Erdogan ‘dictates’ an end to gold imports, imposes tariffs, or confiscates the precious metal?

While physical silver investment demand experienced a pronounced decline this year, the volume is still much larger than the level prior to the 2008 U.S. Housing and Banking Crash. Investors frustrated by a silver market plagued with lousy sentiment and weak demand, may not realize that silver bar and coin demand is projected to be double what it was in 2007.

Thus, long-term precious metals investors continue to acquire silver on price dips while others may be selling out and placing their bets into the bubble stock market or cryptocurrencies. It’s not the larger precious metals investor who is worried about the short-term price, rather its the smaller investor.

Regardless, according to the Silver Institute’s 2017 Interim Report, global silver bar and coin demand are projected to fall to 130 million oz (Moz) in 2017 compared to 206 Moz last year. Even though physical silver investment demand will drop by 37% this year, it will still be more than double the 62 Moz in 2007:

Furthermore, silver bar and coin demand in 2012 was only 29 Moz higher than the estimate for this year, but the price was nearly double at $30 an ounce. As we can see, precious metals investors continued to purchase record amounts of silver bar and coins in 2013, 2014 and 2015 with the hope that prices would eventually start to head higher. However, the majority of the market’s funds since 2012 flowed into STOCKS, BONDS, and REAL ESTATE.

Then after the election of President Trump to the Whitehouse, along with falling precious metals sentiment, investors pulled back on gold and silver investment purchases. From what I have heard through the grapevine, precious metals dealer sales this year are down about 40% across the board. And of course, the massive price increase in Bitcoin and the cryptocurrencies starting in March of this year funneled money away from the metals.

With the new rush of investors into the Bitcoin market mania, several alternative media analysts have given up on precious metals and are now touting cryptocurrencies as the best place to be. In fact, some have stated that gold is no longer useful as a monetary instrument because cryptos will take over this role. Unfortunately, these analysts, just like our mainstream media counterparts, have simply forgotten about the terrible ENERGY PREDICAMENT we are facing. It’s almost as if the lure of $100,000 Bitcoin has totally destroyed their ability to understand that fundamentals still matter…. especially the Falling EROI – Energy Returned On Investment.

Yes, it’s nice to have been one of the fortunate individuals who purchased Bitcoin back when it was $100 (or even less). But, as I stated, the world is still facing a severe energy predicament that Bitcoin or the cryptos can’t solve. When I listen to interviews where analysts say we are moving into a new high-tech world, I wonder where on earth they think we are going to get the energy to run all this stuff. Even though I enjoy watching Sci-Fi movies, it’s totally unrealistic to build spaceships that can be a mile long. The very day after the spaceship is built, all its components and parts start to break down. The more complex the parts, the faster they breakdown.

People need to realize that technology won’t solve our energy predicament, it only makes it worse. Thus, the more complex the technology, the more energy it consumes. So, when someone thinks that, “technology will solve our problems,” then they must also believe in the ENERGY TOOTH FAIRY… a term coined by Louis Arnoux.

I bring up these points because precious metals will still be one the best stores of value in the future as global oil production peaks and declines. We also must remember, the world runs on liquid fuels, not electricity. Even though we see more electric vehicles on the road, they can’t be manufactured without the burning of COAL, NATURAL GAS or OIL. Hence, renewable energy sources such as wind, solar and electric cars are nothing more than fossil fuel derivatives.

Okay, getting back to silver. The GFMS Team at Thomson Reuters, who provide the data for Silver Institute, forecast that global silver production will decline to 870 Moz in 2017:

As we can see in the chart, world silver mine supply peaked in 2015 at 894 Moz and will decrease by 24 Moz in 2017. However, I believe actual global silver production will be less when all the data comes in. Regardless, once the U.S. and worldwide markets finally crack, world silver production will fall even faster. This will be due to the drop in demand for base metals where 58% of global silver production originates (35% byproduct of zinc-lead production and 23% byproduct of copper production).

One segment of the silver market that experienced an uptick was industrial silver fabrication. Global industrial silver fabrication is projected to increase by 19 Moz this year to a total of 581 Moz. However, this increase is still far below the record high of 661 Moz set in 2011:

The majority of the rise in world silver fabrication was due to higher usage in solar PV manufacture and electronics. Even though the global demand for silver by the solar industry will continue to increase over the next few years, it won’t be the driving force in determining the silver price in the future. Instead, the collapse in the value of STOCKS, BONDS, and REAL ESTATE, due to the disintegrating oil industry, will be the factor that forces investors to protect their wealth in gold and silver.

The Federal Reserve was supposed to start unwinding their balance sheet in October. It is now mid-November and the Fed Balance Sheet is growing rather than unwinding.

Keith says the reason the resource markets are lagging is due to institutions not entering the metal market. Until there is a crack in the major markets, we will not see institutional money flow into the mining equities.

The market is quite similar to the year 2000 when it was flat and then took off. History is repeating itself. We need some sort of correction and sane-ness to enter the market. He feels the coming bull market will be quite impressive. He thinks the mining sector over the next decade will become a much more efficient business. Miners will be in a rising metal price environment.

He’s not concerned about being wrong in the short term to be right in the long run. When the market turns, it will turn quickly. The current silver price is almost a joke. We’ve seen lead, zinc, nickel, lithium, and cobalt make significant price rises but gold and silver remain flat. Silver is ignored as a cheap gold substitute, and that is a wrong assumption.

Silver is a strategic metal needed in all sorts of applications, and modern society would not function without it. It’s shocking that this hasn’t been noticed by more people as a result production continues to decline. Platinum metals are not that interesting to Keith as they are small, illiquid markets.

They are quite volatile, and platinum jewelry looks much like silver so why not just buy silver. Now that the world is moving toward electric vehicles he thinks the reasons for owning platinum has declined.

Venezuela officially declared default, no we will have to wait to see what happens next. UK retail is imploding, inflation is spiking and people are being laid off, it is a disaster. 38,000 gold contracts were dumped on the precious metals market. Consumer confidence index unexpectedly declined. Banks are now tightening subprime loans which means this is going to be a disaster for the auto industry. The cabal is still trying to keep the TPP afloat with 11 countries agreeing to terms. Are the rich and the elite panicking because they are hiding money hiring guards.

The only other times in our history when stock prices have been this high relative to earnings, a horrifying stock market crash has always followed. Will things be different for us this time? We shall see, but without a doubt this is what a pre-crash market looks like. This current bubble has been based on irrational euphoria that has been fueled by relentless central bank intervention, but now global central banks are removing the artificial life support in unison. Meanwhile, the real economy continues to stumble along very unevenly. This is the longest that the U.S. has ever gone without a year in which the economy grew by at least 3 percent, and many believe that the next recession is very close. Stock prices cannot stay completely disconnected from economic reality forever, and once the bubble bursts the pain is going to be unlike anything that we have ever seen before.

If you think that these ridiculously absurd stock prices are sustainable, there is something that I would like for you to consider. The only times in our history when the cyclically-adjusted return on stocks has been lower, a nightmarish stock market crash happened soon thereafter…

The Nobel-Laureate, Robert Shiller, developed the cyclically-adjusted price/earnings ratio, the so-called CAPE, to assess whether stocks are likely to be over- or under-valued. It is possible to invert this measure to obtain a cyclically-adjusted earnings yield which allows one to measure prospective real returns. If one does this, the answer for the US is that the cyclically-adjusted return is now down to 3.4 percent. The only times it has been still lower were in 1929 and between 1997 and 2001, the two biggest stock market bubbles since 1880. We know now what happened then. Is it going to be different this time?

Since the market bottomed out in early 2009, the S&P 500 has been on a historic run. If this rally had been based on a booming economy that would be one thing, but the truth is that the U.S. economy has not seen 3 percent yearly growth since the middle of the Bush administration. Instead, this insane bubble has been almost entirely fueled by central bank manipulation, and now that manipulation is being dramatically scaled back.

And the guys on Wall Street know what is coming. For example, Joe Zidle says that this bull market is now in “the ninth inning”…

Joe Zidle, of Richard Bernstein Advisors, is arguing that the bull market has entered the bottom of the ninth inning.

“This is a late-cycle environment,” Zidle said on CNBC’s “Futures Now” recently.

“In innings terms, they’re not time dependent. An inning could be shorter or they could be longer. It just really depends,” the strategist said.

This bubble has lasted for much longer than it ever should have, and everyone understands that a day of reckoning is coming.

In fact, earlier today I came across an article on Zero Hedge that contained an absolutely remarkable quote from Eric Peters…

“We are investing as if 1987 will happen tomorrow, because it will,” said the CIO. “But we need to be long, or we’ll be out of business,” he explained, under pressure to perform. “So we construct option trades that are binary bets.” Which pay X profit if stocks rally, and cost Y if markets fall. No more and no less.

“What you do not want is a portfolio whose losses multiply depending on the severity of a decline.” That’s what most people have today. “At the last stage of the cycle, you want lots of binary bets. Many small wins. Before the big loss.”

“Are we at the start or the end of the ‘Don’t know what I’m buying’ cycle?” asked the same CIO. “No one knows.” But we’re definitely within it.

“When their complex swaps drop 40%, and prime brokers demand more margin, investors will cry ‘It’s not possible!’ But anything is possible.” The prime brokers will hang up and stop them out.

In case you don’t remember, in 1987 we witnessed the largest one day percentage decline in U.S. stock market history.

When it finally happens, millions upon millions of ordinary Americans will be completely shocked, but most insiders know that the other shoe is going to drop at some point.

In particular, watch financial stock prices very closely. Last month, Richard Bove issued a chilling warning about bank stocks…

One of Wall Street’s most vocal bank analysts is troubled by the rally in financials.

The Vertical Group’s Richard Bove warns that the overall market is just as dangerous as the late 1990s, and he cites momentum — not fundamentals — as what’s driving bank stocks to all-time highs.

“If we don’t get some event in the economy or in politics or in somewhere that is going to create more loan volume and better margins for the banks, then yes, they would come crashing down,” Bove said Monday on CNBC’s “Trading Nation.” “I think that the risk in these stocks is very high at the present time.”

It isn’t going to take much to set off an unstoppable chain of events. Our financial markets are even more vulnerable than they were in 2008, and the right trigger could unleash a crisis unlike anything we have ever seen in modern American history.

Unfortunately, most Americans keep getting fooled by the artificial boom and bust cycles that the central banks create. Right now most people seem to have been lulled into a false sense of security, and they truly believe that everything is going to be okay.

But every time before when the market has looked like this a crash has always followed, and this time will be no exception.

Former Federal Reserve Chairman Alan Greenspan is the latest high profile financer to give his take on the controversial currency. In an exclusive interview on FOX Business Network’s “Mornings With Maria,” Greenspan said “Bitcoin is what used to be called fiat money.” He then compared Bitcoin to the currency issued by the Continental Congress after the American Revolution began.

“I would use the analogy of Continental currency. Continental currency in 1775 was issued with no backing and it sold at par in the marketplace for quite a while until they started to build up more and more printing of continentals.”

According to Greenspan, the perception of the cryptocurrency is not necessarily matching the reality, saying, “Human nature is such that if you get something such as Bitcoin, you think there is some value there whether there is or there isn’t. But that’s the same thing as a Continental, greenbacks in the Civil War, all of these currencies which didn’t have any backing.”

Washington DC is not buzzing with activity so that taxpayers can be permitted to keep more of their earnings. Washington and the surrounding areas are some of the richest places in the entire country.

While it may appear that government cuts taxes in one area, they always make sure to raise them in another. A new philosophy on the role of government is desperately needed. Ron Paul discusses on today’s Liberty Report.

George Milling-Stanley of State Street says in a run-up to a rate hike, investors tend to short gold, but any Fed hikes next year shouldn't derail prices.

Physicists say that the universe is expanding. However, they hotly debate (OK, pun intended as a foreshadowing device) if the rate of expansion is sufficient to overcome gravity—called escape velocity. It may seem like an arcane topic, but the consequences are dire either way. If the rate of expansion is too low, then it will get slower and slower until expansion stops entirely, then finally, begin collapsing again in a Big Crunch. That’s bad enough. But the other possible fate of the universe is even worse. If the expansion is fast enough, then the universe will keep expanding forever. Things will get colder and colder, until the state called the heat death occurs.

If only economics had similarly vigorous controversies. It faces its own existential problems. For example, there is an analogous concept to heat death in the economics universe. Will credit continue to grow, and with it the economy? Or will some force—or law of economics—prevent slow and stop it?

There is a force that can cause the heat death of the economic universe. It is not the moralizing argument that faults man for the sin of wanting more material comfort, and condemns his desire for growth as hubris.

Everyone needs growth. Even the environmentalists couch their anti-growth policies. They want us to stop using energy, but cannot openly promote energy poverty as an ideal. So they talk in terms of sustainability.

Sustainability is an interest concept. For a process or system to be sustainable, it means that there is no reason why it cannot continue indefinitely (well at least until the sun goes red giant and engulfs the Earth, which may not happen because before that our galaxy is on a collision course with the Andromeda galaxy…)

Well, is our economy and its monetary system sustainable? How do you even approach this question in a rigorous way?

We submit one fact for your consideration. To service debt, you must generate income. If you fail to pay at least the interest when due, then the creditors suffer big losses. This impairs their capacity and appetite to lend to others, which suffocates businesses who need capital to expand. So the key is generating enough income to pay interest. We would add on top of that the need to amortize the principal too.

The analogy to heat death of the universe is a pretty good fit. Physicists are not looking at one probe that is moving out of the solar system and will chill down to near absolute zero when its power supply runs out of juice. Nor one object, such as Pluto. They are looking at the universe and all entities in it including all stars and all life on all planets.

Similarly, we as economists must look at the economic universe and all business enterprises and people in it. If one business is stranded with, e.g. an obsolete product such as mobile phone that can only do voice calls, it will fail and default on its debts. That is not under question. The question is: can it happen to the entire economy? If it does, then the monetary system will fall and everyone will lose their savings.

If it can happen what are the circumstances?

So far, we said income (that is net income, after cost of goods sold and all other expenses) must exceed debt service. And, perhaps including debt amortization.

Measuring these two quantities, much less estimating them years or decades in the future, would be quite a challenge. Just like measuring the velocities and distances of all objects in the universe.

Fortunately, we can look at something much easier. We know the economy is in motion today. So we just need to know the trend. If income is rising at least as fast as debt service, then we can say that the economy is sustainable.

We have been writing about this trend for the last month, though we did not describe it in this context. The variable we need to measure is none other than marginal productivity of debt! MPoD, as we will call it here for brevity, is a measure of how much new GDP is added for each freshly borrowed dollar.

The graph we published on Oct 15 is included again here.

Aside from the anomaly when MPoD moved up sharply in the wake of the great financial crisis (which we discussed here), it is an unmistakable falling trend. Post 2010, it is falling again from that higher level. This trend spans many decades, and it is no fluke.

A falling MPoD means we get less and less GDP for each borrowed dollar. Or conversely, we have to borrow more and more dollars to get a dollar of GDP. This is significant as growth in net income can be no greater than growth in GDP (but it is likely a lot slower, a whole ‘nother topic). This graph is saying that the income to debt ratio is falling.

We are getting close to our statement above, income must exceed debt service or else there will be a heat death of the economic universe. We have now proven income is growing slower than debt total. We have one more step, to prove income is growing slower than debt service.

Normally, debt service would grow proportionally with debt. It may seem fortunate that we don’t live in a normal universe, as we shall see in a moment. We live in an abnormal place, which is subject to one of the planks proposed by Karl Marx in his infamous Communist Manifesto.

“5. Centralisation of credit in the hands of the state, by means of a national bank with State capital and an exclusive monopoly.”

The central bank conducts what it calls monetary policy. The net result of monetary policy for 36 years so far is falling interest rates. Keith has written about the various ways that falling interest causes destruction in his series of articles on yield purchasing power.

However, in light of the heat death question, falling interest would seem to have the potential to save us. It is obvious that servicing the same debt at 1% interest has a lower monthly payment than at 10%. This is why many economists say there is no problem. We are told that, “debt service today is not a greater percentage of GDP than it was when the debt was much lower decades ago.” That may be true, and we won’t even get into if net income is the same percentage of GDP as it was (we would bet an ounce of fine gold against a soggy dollar bill it isn’t).

We want to make a different argument. If debt service depends on falling interest, what happens when interest hits zero? Here is another good analogy to physics, which also asks what happens at zero. In physics, nothing. Literally. Motion stops on even a molecular level at absolute zero.

What happens to an economy when interest—we mean the long-term bond rate—falls to zero? What happens when businesses can borrow at 0%? Well, obviously, debt service goes to zero (not including amortization of the principal). With no cost to borrow, businesses can borrow for activities that produce no economic value(!)

In a normal economic universe, interest is greater than zero. As we said last week:

“A dollar to be paid next year is worth less than a dollar in the hand today. One reason is that we are mortal beings. In order to be alive next year, we must remain alive every single day between now and then. There are natural reasons for time preference—the desire to have a good today, and not postpone it. We are also not omniscient. Something may come up, such as an illness, which forces us to consume what we did not plan to consume.

Another reason is, of course, risk. Unlike the magic machine in our example, a business enterprise may cease to make money for any number reasons including a new competitor or changing customer preferences.

For many reasons, a dollar to be paid next year is not worth a dollar today. A dollar to be paid in ten years is worth even less. Future payments must be discounted. The discount is related to the interest rate, and it shares many of the same causes.”

At zero, this economic law is violated. No one can act as if he had no time preference, which is exactly what zero interest requires him to do.

And zero, itself, is not sustainable anyway. Assuming that some amount of amortization is required, then the debt service becomes unbearable and the interest rate must keep falling.

When interest is positive, or even zero, business borrowing must fund activities that generate a positive return (even if only share buybacks). However, when interest goes negative, they can borrow to engage in capital-destroying activities. So long as the rate of destruction is below the rate of interest.

For example, suppose an enterprise destroys its investors’ capital at 1% per year. That’s bad. But what if it can borrow this capital at -2%? The investors lose 2% per year. But the business nets +1%. Positive one percent. What is profitable to do, will be done at large scale across the entire economic universe.

At negative rates, investors lose a bit of their capital every year. They are subsidizing businesses who are destroying it bit by bit every year.

Negative interest rates are not sustainable. A falling interest rate can make debt service cheaper. However, it does not solve the problem of falling marginal productivity of debt. The heat death of the economic universe looms closer every day (we make no prediction of the timing of this here, that will be the subject of a future series).

So now we can write an economic law:

If MPoD < 1, the economy is unsustainable

That is, the heat death of the economic universe is inevitable.

Note that MPoD was under 1 even as long ago as the 1950’s (we suspect this pathology began either around the time of President Roosevelt’s gold confiscation in 1933, or the creation of the Federal Reserve in 1913, but we don’t have the data going back that far).

Prior to the crisis of 2008, MPoD fell below 0.1. Even now with its post-crisis boost, it is well under 0.4, and falling.

It is time for gold to enter the mainstream monetary discussion. Interest rates and MPoD do not fall when there is a free market in money and credit. And the market will choose gold, if it is free to do so.

The prices of the metals ended all but unchanged this week, though they hit spike highs on Thursday. Particularly silver his $17.24 before falling back 43 cents, to close at $16.82.

It was not a gentle fall back. In about an hour and fifteen minutes on Friday morning (as we Arizonans reckon the time), the price of silver dropped from $17.16 to $16.76. Was this a case of the infamous manipulation we’ve all read about? We can’t tell you who did it, but we can show you a clear picture of what happened.

In any case, it seems that either Fed Chairman Appointee Powell is not good for silver, or else that the price of silver has little to do with continuation of current Fed (central) planning.

We will look at intraday gold and silver supply and demand fundamentals. But first, here are the charts of the prices of gold and silver, and the gold-silver ratio.

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio fell a hair.

In this graph, we show both bid and offer prices for the gold-silver ratio. If you were to sell gold on the bid and buy silver at the ask, that is the lower bid price. Conversely, if you sold silver on the bid and bought gold at the offer, that is the higher offer price.

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph showing gold basis and cobasis with the price of the dollar in gold terms.

We see a rising cobasis (our measure of scarcity) along with a rising price of the dollar (i.e. falling price of gold, in dollar terms). This is not surprising; it is the typical pattern nowadays.

We also see the cobasis tracking the price of the dollar. Look at how they go down together on Wednesday and Thursday, and up together on Friday. Keep in mind that the contract roll is well underway, that it impacts the silver basis more than the gold basis. Mechanically, the roll involves selling the expiring contract.

Jay Taylor and John Rubino discuss thoughts on the increase in the money supply, velocity of money and what it means for the Fed’s monetary policy in light of debt levels.

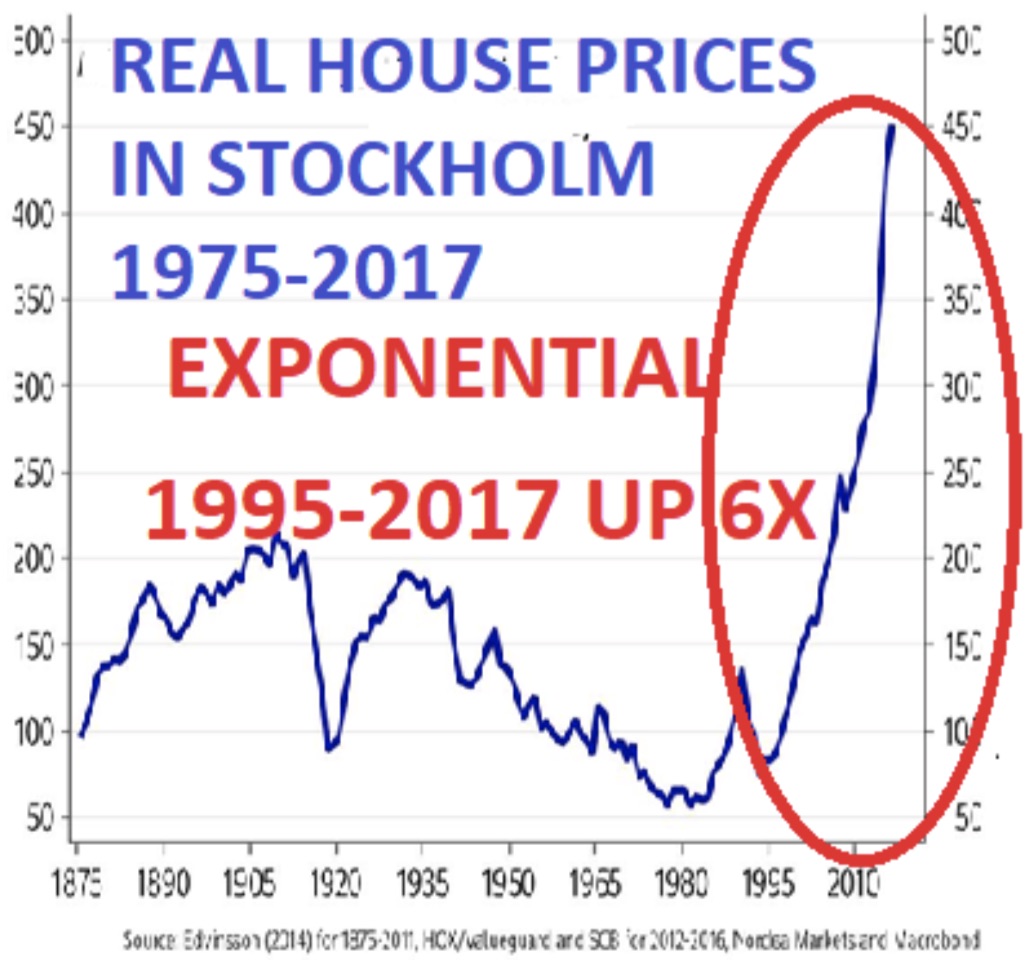

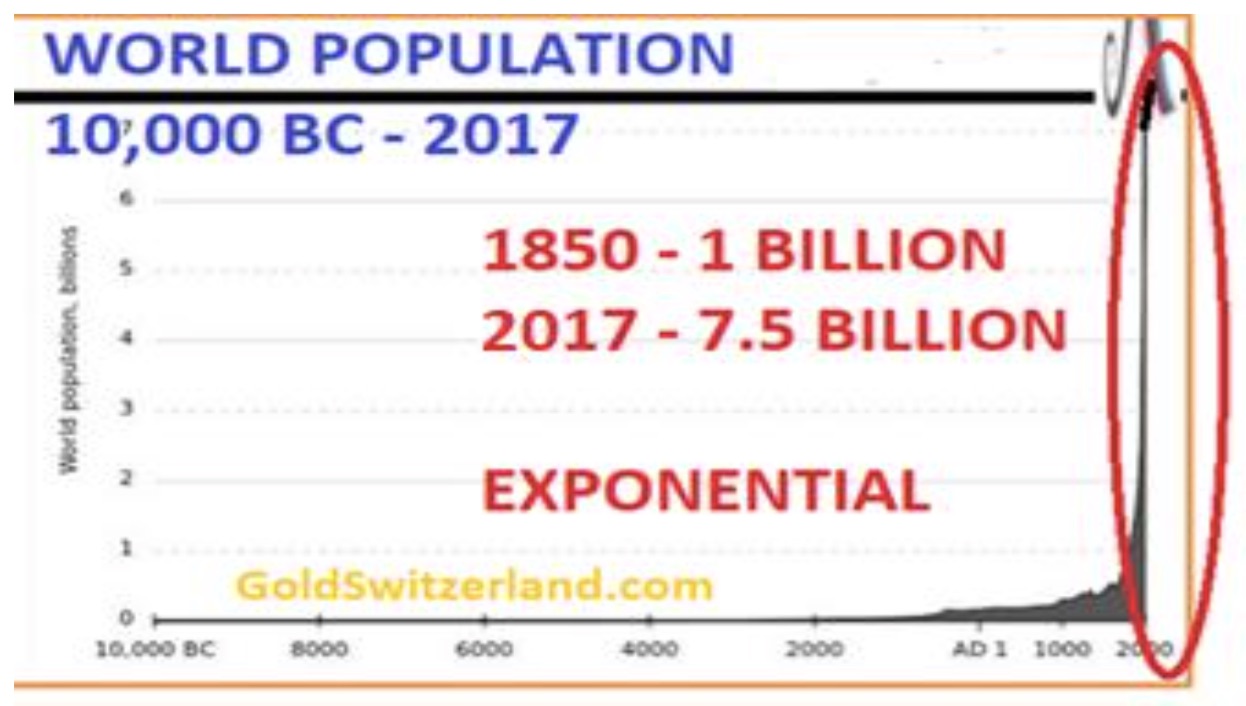

Egon von Greyerz: “We are currently standing before one of the most unique and frightening periods in history. Never have there been so many extremes in so many different areas. In the last 100 years everything seems to have grown and intensified much faster, including population, technology, inflation, debt, money printing, budget deficits, stocks, bonds, property prices. cryptocurrencies etc…

“All of these areas are now in an exponential growth phase. The final stage of exponential growth is explosive and looks like a spike that goes straight up. A spike for a major sample like global population or the Dow never finishes with just a sideways move. Once a spike move has finished, it always results in a spike move down.

It seems that everything in the world is developing much faster today, such as computers and mobile phones or robots. The world assumes that this exponential growth in so many areas will continue or even accelerate further. But sadly, that is unlikely to be the case.

There is a more scientific illustration of how these exponential moves occur and also how they end.

Imagine a football stadium which is filled with water. Every minute one drop is added. The number of drops doubles every minute. Thus it goes from 1 to 2, 4, 8, 16 etc. So how long would it take to fill the entire stadium? One day, one month, or one year? No, it would be a lot quicker and only take 50 minutes! That in itself is hard to understand, but even more interestingly, how full is the stadium after 45 minutes? Most people would guess 75-90%. Totally wrong. After 45 minutes the stadium is only 7% full! In the final 5 minutes the stadium goes from 7% full to 100% full.

That is the simple explanation why we are seeing this very fast exponential move in so many areas. It is of course impossible to say exactly when the global stadium or individual stadiums will be filled especially since we don’t know the size of these stadiums. What we do know is that when it is full, the water level will not only stop rising but the stadium will collapse.

We are probably now in the final minute, or probably seconds, of the move since we are in the exponential phase that has lasted around 100 years.

If we look at a few examples of exponential growth, we can start with world population. For thousands of years global population grew very slowly but finally reached 1 billion in the 1850s. Since then it has gone up over 7x to 7.5 billion. Many “experts” now forecast that we will soon reach 15 or 20 billion.

Yes, global population could grow slightly from here but more likely is that we will see a major reduction in the coming decades. It could even happen a lot faster depending on the type of event that the world is facing. Looking at the size of the exponential move, 6.5 billion people have been added to world population since the mid 1850s. A normal correction to such an exponential growth would be 38% to 50%. This would mean that world population could go down between 2.5 and 3.7 billion to 3.8 to 5 billion people. This clearly sounds horrendous and improbable but looking at the chart, it is likely to happen. It is of course possible that we could see some further growth before global population goes down. But the risk of the downturn starting soon is much greater than a significant further increase.

The triggers for such a major reduction could be manifold like war, epidemic disease, economic collapse leading to poverty and famine or a combination of these events. For example, around 1340-50 there was the Black Plague that reduced the European population by up to 60% and world population by an estimated 30 to 50%. A nuclear war between North Korea and the US would eventually involve China, Russia, Iran, Pakistan, India and many other countries and would be just as devastating, probably leading to world population going down by much more than 60%. Likewise, a collapse of the financial system, which is not improbable, would be cataclysmic for the world.

It is absolutely clear that one or several of these events will take place in coming years but when exactly is of course impossible to say. Depending on the magnitude of the problem, including the geographical spread, it is very difficult to prepare for it for normal people. Very few have their private jet and residences in many parts of the world. However, for people who have savings, now is the time to take defensive measures if you haven’t already. I know of very old family wealth who for hundreds of years have kept their wealth in property, art and gold with 1/3 in each. With productive land, this has of course been a superb portfolio and will continue to do very well during the coming downturn. Gold and agricultural land are real wealth preservations assets, while some art today is a bubble asset and therefore will suffer. But 2/3 of the assets are likely to perform extremely well in coming years.

A contrarian or a risk averse investor can today look at any chart of stocks, bonds or property, which will all tell him that we are now at extremes. On a risk/reward basis, very few investors make money by buying at the very final stages of a move. Yes, it is true that anyone who bought into the Nasdaq in early 1999 had more than doubled his money by March 2000. The problem is that more than 95% of investors stayed in at that point and most did not get out until they had lost 50-80%.

As the superb Chairman of Sprott USA, Rick Rule, stated at the New Orleans Investment Conference last week: “Either you are a contrarian or you will be a victim.” The reality is that most people will be victims in coming years. Very few will realize that what we will see next is the end of a major era or cycle of a major degree. Whether it is a 300 year cycle or a 2,000 year cycle doesn’t really matter. Historians will know afterwards. What we need to focus on today is to protect ourselves against these risks rather than to become victims.

Back in 2002, we decided as a company that risk in the world would accelerate in coming years and it was the right time to protect ourselves and our clients. Gold at that time was unloved and undervalued. It had been going down for 20 years and nobody was interested. Gold bottomed in 1999 at $250, having gone down from the $850 peak in January of 1980.

The average investor obviously did not get very excited that gold had gone up $50 since 1999, and was $300 in February 2002. That was when we decided to put a significant percentage of our own funds into gold as well to recommend to our investors to do the same.

This is a typical contrarian investment. You buy an asset that is on nobody’s radar screen, and in the case of gold in 2002, 65% below its peak price 22 years earlier. But it is of course not enough just to buy something which is cheap. What you buy must also have an intrinsic value and the potential to grow substantially. Gold’s role as the only money that has existed and survived for almost 5,000 years makes it clear that function is likely to continue for many thousand of years to come.

Also, Greenspan’s easy money policy had started in 1987 when Fed Funds reached 10%. With a weak economy, and weak asset markets Greenspan started his stimulative policy and lowered rates down to 3% in 1992. They had gone under 2% in early 2002 when we bought gold. Eventually rates came down to 1% on Greenspan’s watch. When Bernanke then needed to sort out the mess during the great financial crisis, rates were lowered form 5% in 2007 to 0% in 2009 where they stayed until 2015.

The income tax should be 0%, just as it was for the first 137 years of American history. So tax cuts across the board are always a welcome development. However, tax cuts are just part of the big picture. What we need is a total cut in government's size and scope. Unfortunately, President Trump is not going in that direction.