- Source, Wolf St Report

Monday, 30 December 2019

Saturday, 21 December 2019

Dennis Meadows: The Limits To Growth

In 1971, its findings were first released in Moscow and Rio de Janeiro, and later published in 1972 under the title The Limits To Growth. Few reports have generated as much debate, discussion and disagreement.

Though it’s hard to argue that its forecasts made back in the early 1970s have proved eerily accurate over the ensuing decades. But most of its warnings have been largely ignored by policymakers hoping (blindly?) for a rosier future.

One of the original seventeen researchers involved in The Limits To Growth study, Dennis Meadows, joins us for the podcast this week. Fifty years later, what does he foresee ahead?

- Source, Peak Prosperity

Friday, 20 December 2019

Keith Weiner: Euthanasia of Capitalism by the Federal Reserve Bank

- Source, Jay Taylor Media

Thursday, 19 December 2019

The Decade of the Central Bank is Coming to An End

On Nov. 25, 2008, the Federal Reserve launched the shot heard around the financial world.

The central bank announced it would start using digitally created money to buy mortgage debt in an effort to drive down interest rates and resuscitate a dead housing market.

Along with a series of cuts that ultimately would take short-term interest rates close to zero, the move was part of an ambitious gambit to take the country out of its worst economic crisis since the Great Depression. It quickly expandedto the purchase of government bonds in a total of three rounds that spanned six years.

Flash forward 11 years.

The Fed’s campaign of “quantitative easing,” along with keeping rates historically low, coincided with the longest expansion and most robust Wall Street bull market in U.S.history . Coming at a time of prolonged gridlock in Washington, the Fed’s monetary policy moves thrust it front and center as the sole provider of stimulus.

“It was the decade of the central bank,” said Quincy Krosby, chief market strategist at Prudential Financial. “Stimulus was wanting, and the burden fell on the central banks to normalize the environment.”

Economists can and will debate the effectiveness and the long-term consequences of all the extraordinary moves, but there can be little doubt that in the past decade, the epicenter of economic management was at the Fed, along with its sister central banks around the globe.

No collective entity hadgreater influence for the past 10 years over the economy and financial markets.

‘The extraordinary has become ordinary’

While the desire may have been a normalization of a global economy that had been crushed by a speculative real estate bubble, the measures taken to achieve that goal were anything but normal.

Central banks cut borrowing rates more than 50 times over the past decade and instituted “money printing” QE programs to the tune of nearly $11 trillion just between the Fed, the European Central Bank and the Bank of Japan. Never before had these institutions been called upon by so many to do so much. But lacking other fiscal measures — government spending on capital projects and the like — there was little alternative.

Former Fed Chairman Ben Bernanke even half-joked once that such programs don’t work in theory but do in practice, part of the general reluctance central bankers had to such aggressive intervention. His successor, Janet Yellen,put a halt to the money printing and began the process of gingerly rolling off the bond portfolio acquired through the three rounds. Now, she continues to defend the Fed’s stimulus actions during and after the financial crisis.

“After all, the economic consequences of what we had were really quite terrible,” Yellen said recently at a World Business Forum conference in New York. “This was a very serious thing, but it could have been the Great Depression. My colleagues and I knew that it wason us to figure out what we needed to do to make this the Great Recession rather than the Great Depression.”

The central bank announced it would start using digitally created money to buy mortgage debt in an effort to drive down interest rates and resuscitate a dead housing market.

Along with a series of cuts that ultimately would take short-term interest rates close to zero, the move was part of an ambitious gambit to take the country out of its worst economic crisis since the Great Depression. It quickly expanded

Flash forward 11 years.

The Fed’s campaign of “quantitative easing,” along with keeping rates historically low, coincided with the longest expansion and most robust Wall Street bull market in U.S.

“It was the decade of the central bank,” said Quincy Krosby, chief market strategist at Prudential Financial. “Stimulus was wanting, and the burden fell on the central banks to normalize the environment.”

Economists can and will debate the effectiveness and the long-term consequences of all the extraordinary moves, but there can be little doubt that in the past decade, the epicenter of economic management was at the Fed, along with its sister central banks around the globe.

No collective entity had

‘The extraordinary has become ordinary’

While the desire may have been a normalization of a global economy that had been crushed by a speculative real estate bubble, the measures taken to achieve that goal were anything but normal.

Central banks cut borrowing rates more than 50 times over the past decade and instituted “money printing” QE programs to the tune of nearly $11 trillion just between the Fed, the European Central Bank and the Bank of Japan. Never before had these institutions been called upon by so many to do so much. But lacking other fiscal measures — government spending on capital projects and the like — there was little alternative.

Former Fed Chairman Ben Bernanke even half-joked once that such programs don’t work in theory but do in practice, part of the general reluctance central bankers had to such aggressive intervention. His successor, Janet Yellen,

“After all, the economic consequences of what we had were really quite terrible,” Yellen said recently at a World Business Forum conference in New York. “This was a very serious thing, but it could have been the Great Depression. My colleagues and I knew that it was

- Source, CNBC

Tuesday, 17 December 2019

Alan Greenspan: Inflation is Inevitably Going to Rise

“Right now, there’s no real inflation at play. But if we go further than we are currently, inflation is inevitably going to rise,” the ex-central bank chief said Tuesday on CNBC’s “Squawk on the Street.”

As things stand, the U.S.

That has come even though the 3.5% unemployment rate is the lowest it’s been in 50 years. Fed economists closely watch what is known as the Phillips Curve, which traditionally has indicated that lower inflation will drive higher wages and push inflation gauges up simultaneously.

The U.S.

“That, on top of the stagnation we are seeing in many areas, is not very beneficent for the world economy and certainly not for the United States and China,” Greenspan said.

The deficit has continued to swell under President Donald Trump, going from $665 billion during his first year in office in 2017 to this past year’s $984 billion, a jump of nearly 50%.

- Source, CNBC

Sunday, 15 December 2019

Gold Confiscation? Is Jewelry a Good Backup Plan?

That’s how Mike Maloney begins his new video, a discussion with Jeff Berwick of Dollar Vigilante, on the possibility of gold confiscation.

While Mike says confiscation “probably won’t happen, you’re screwed if all you own is coins and bars.” In other words, the risk isn’t zero.

As many investors know, gold was illegal to own in the US for 50 years. Is there a way for an investor to hedge against such an event? Gold Bullion Jewelry might be a solution.

As Mike says, “gold bullion jewelry is meant to give mobility and safety, and is the least likely form of precious metals to be nationalized.” It’s ideal for travel, because, as Mike points out, “it doesn’t have to be declared on a landing card.”

Customs forms specifically ask about currency and cash equivalents—but jewelry is not classified as a financial instrument. As a result, he owns some gold jewelry as a tail risk.

- Source, Gold Silver

Friday, 13 December 2019

Wednesday, 11 December 2019

Ron Paul: The Fed's Inflation is Coming, Get Ready for It

The Fed has inflated the money supply to astronomical levels, and they keep creating hundreds of billions more out-of-thin-air. When it shows up in higher prices, it shouldn't surprise anyone.

- Source, Ron Paul

Monday, 9 December 2019

John Williams: Fed Lost Control of the Financial System

If they understood what was going on, they would not be doing that. They wouldn’t have to do it. They have lost control of the system effectively,” says Williams. Williams goes on to say, “It tells you the underlying system is unstable. I can see where the economy is based on the hard numbers even though they do funny things with the numbers.

We are seeing a very weak economy here. Again, the Fed tightened and they eased to help the banks, but they did not do much to help the economy.

The banks are not as healthy as they appear and as they have been promoted. The Fed may well be on the brink of the type of crisis they had back in 2007.”

- Source, USA Watchdog

Wednesday, 4 December 2019

Frank Holmes: Are You Horribly Under-invested in Gold?

- Source, Jay Taylor Media

Sunday, 1 December 2019

Enormous Amounts of US Corporate Bond Maturities Coming Due In The Next Few Years

The amount of corporate debt issued is growing over hundreds of billions of dollars per year thanks to over $700 billion dollars worth of share buybacks with debt, leveraged loan and collateralized loan obligation (CLO) growth and ratings agencies refusing to downgrade an absolutely enormous amount of corporate debt rated as BBB that should not be rated that high.

- Source, Wall St for Main St

Tuesday, 26 November 2019

Ray Dalio and central banks turn to gold, prepare for crisis

While the Federal Reserve seems to hold a neutral view of the economy in the medium-term, prominent investors like Ray Dalio, as well as central banks, are stockpiling safe haven and hedge assets to prepare for what they believe is a coming economic downturn, this according to Phil Streible, senior market strategist of RJO Futures.

“One of the guys who I really follow, Ray Dalio and Bridgewater, they came out and bought about a billion dollars worth of put options in the S&P 500, so that tells you that these guys are preparing for some kind of crisis,” Streible told Kitco News.

- Source, Kitco News

Monday, 25 November 2019

The Vigilante's View on Gold, Crypto, Manipulation, Health and Wealth

- Source, The Dollar Vigilante

Saturday, 23 November 2019

Serbia’s gold buying may mean a lot more than you think

- Source, Kitco News

Friday, 22 November 2019

Robert Moriarty: Has Novo Resources Made the Gold Discovery of the Century?

- Source, Jay Taylor Media

Thursday, 21 November 2019

Here’s the secret to owning perfect amount of gold

“We have found that the efficient level, the optimized level, was 35% gold. Not saying you should own 35% gold, that’s an awfully high concentration, but it challenges the conventional wisdom of what pertains to gold and how to use it,” Giannotto told Kitco News.

- Source, Kitco News

Wednesday, 20 November 2019

How 2019's Market Top Parallels to the Time Right Before the 2008 Financial Crisis

Henrich argues that with or without complete central bank capitulation, markets are in for a year-end rally that will not be able to sustain or surpass its new highs.

He compares the final months of 2019 to the final months of 2007, pointing out the critical divergence in the Fed’s ability to lower interest rates further - having less than half the wiggle room than the 500 basis points they had in 2007.

- Source, Real Vision Finance

Tuesday, 19 November 2019

Gold and Silver Will Head Higher and This is Where I’m Investing My Money

He cautions that some gold pundits focus too much on the supply-demand characteristics of gold while missing the bigger picture that gold is primarily a safe-haven asset.

When there is blood in the streets, there is no correct price for gold. He sees the current gold correction as an opportunity that investors should not miss, and some big names are getting involved in the marketplace.

Also, investors should be aware of the current events happening in uranium and the supply issues with nickel.

- Source, Palisade Radio

Monday, 18 November 2019

The gold versus bitcoin debate is still on, expert says $20k is in the cards but for which?

“I think that bitcoin can easily go to $20,000, I’m expecting it to go to $50,000,” Chambers told Kitco News.

- Source, Kitco News

Thursday, 14 November 2019

Stocks Struggle Amid Barrage Of Dismal Econ Data, HK Violence As Germany Narrowly Avoids Recession

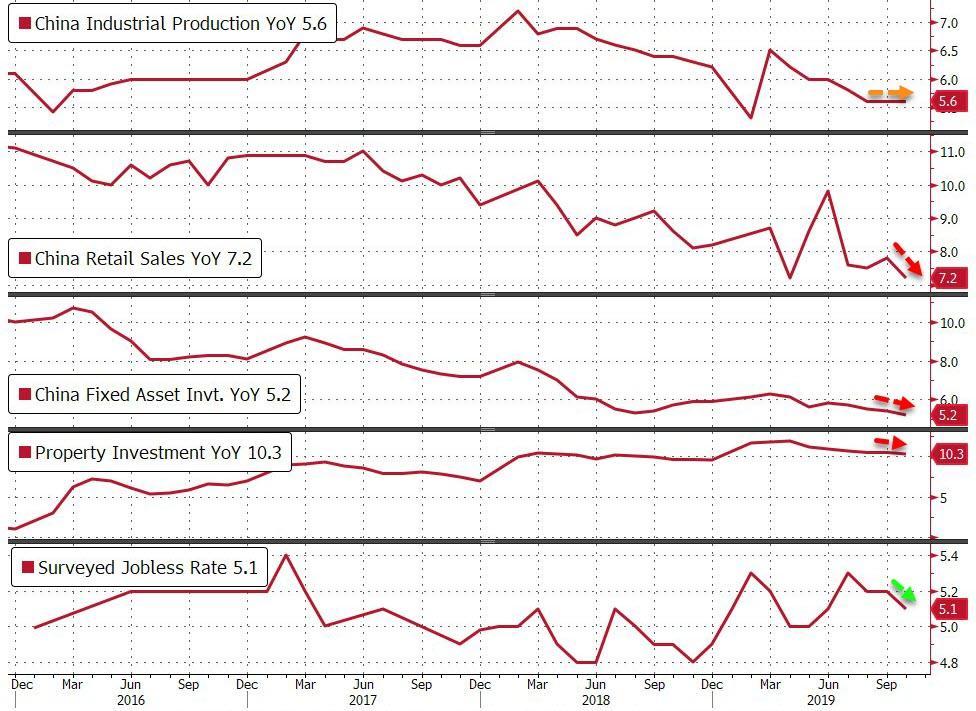

Global stocks and US equity futures eased further on Thursday as the latest dismal Chinese data missed across the board and showed further economic slowdown , with investment growth printing weakest since 1998...

...adding to worries about the global growth fallout from the U. S. -China trade war. U.S. futures were down 0.14%, following a record-high close on the S&P 500 on Wednesday. Futures bounced briefly after news that China customs have lifted restrictions on US poultry meat imports, with China's Global Times acknowledging saying the move comes "amid the continuation of tradetalks , paving the way for hundreds of millions of dollars worth US meat export to China"; the US exported $390MM worth of poultry to China in 2014 before the ban. Yes, million, not billion.

With earnings season ending, Cisco Systems tumbled in early trading after its quarterly sales forecast fell far short of projections, while WalMart surged after the company raised its full year outlook. Altice Europe NV beat earnings estimates, while Burberry GroupPlc climbed after reporting six-month earnings that exceeded expectations.

The MSCI All-Country World index was down 0.14% afterstart of trading in Europe. European shares initially fell, but later rebounded after data showing the German economy just barely missed a recession, rising 0.1% in the third quarter, avoiding a contraction thanks to consumer spending, and beating expectations of a second consecutive contraction.

While a recession was averted, the news was hardly good as Germany grew at just half the pact of the overalleurozone as growth across the entire continent grinds to a halt.

“Obviously it’s better than expected, but actually I would argue is that it’s a hollow victory because in effect it makes a fiscal response less likely,” said Michael Hewson, chiefmarkets analyst at CMC Markets in London. “I think if they’d gone into a technical recession, the pressure to loosen the purse strings so to speak would have been much much greater.”

In Asia, stocks fell after very poor economic data in China and Japan showed the trade war between Beijing and Washington was hitting growth in some of the world’s biggest economies. MSCI’s broadest index of Asia-Pacific shares outside Japan fell 0.3%, while Japan’s Nikkei index fell further, dropping 0.8%. Asian stocks slid for a second day, led by material producers, as China’s economy slowed further in October, with factory output, retail sales and investment all below estimates. Most markets in the region were down, with Japan leading declines. The Topix fell 0.9%, dragged down by Sony and Toyota Motor, as Japan’s economy slowed sharply in the third quarter amid shrinking exports. Q3 GDP in Japan printed at just 0.1% - the same as Germany - and missing estimates of 0.2%.

...

With earnings season ending, Cisco Systems tumbled in early trading after its quarterly sales forecast fell far short of projections, while WalMart surged after the company raised its full year outlook. Altice Europe NV beat earnings estimates, while Burberry Group

The MSCI All-Country World index was down 0.14% after

While a recession was averted, the news was hardly good as Germany grew at just half the pact of the overall

“Obviously it’s better than expected, but actually I would argue is that it’s a hollow victory because in effect it makes a fiscal response less likely,” said Michael Hewson, chief

In Asia, stocks fell after very poor economic data in China and Japan showed the trade war between Beijing and Washington was hitting growth in some of the world’s biggest economies. MSCI’s broadest index of Asia-Pacific shares outside Japan fell 0.3%, while Japan’s Nikkei index fell further, dropping 0.8%. Asian stocks slid for a second day, led by material producers, as China’s economy slowed further in October, with factory output, retail sales and investment all below estimates. Most markets in the region were down, with Japan leading declines. The Topix fell 0.9%, dragged down by Sony and Toyota Motor, as Japan’s economy slowed sharply in the third quarter amid shrinking exports. Q3 GDP in Japan printed at just 0.1% - the same as Germany - and missing estimates of 0.2%.

- Source, ZeroHedge , read more here

Wednesday, 13 November 2019

Rob Kirby: Amount of Money Fed Into System Now Too Hard to Hide

Macroeconomic analyst Rob Kirby goes on to warn, “Gold and silver are historically alternatives to a failing fiat currency regime.

The U.S. dollar is failing in front of our eyes. We know that because we know that $21 trillion extra (on top of the $23 trillion national debt) was created, and we know what they are doing with it. Part of that $21 trillion is being used to knock the price of gold and silver down with paper contracts.

This is not a winning strategy, and this will ultimately blow up in their face too. They are being done to buy time and make the dollar appear strong.

The way this has to end is the U.S. dollar will go to its real intrinsic value, which is zero. That implies a hyperinflationary experience at some point in time, and it could be soon.

The amount of money being fed into the system is soon going to be too hard to hide.”

- Source, USA Watchdog

Russia to cut share of U.S. dollar in National Wealth Fund, mulls other currencies

Russia will reduce the share of the U.S. dollar in its National Wealth Fund and is considering investing in other foreign currencies including the Chinese yuan, Deputy Finance Minister Vladimir Kolychev said on Wednesday.

The U.S.

“Geopolitical risks are one of the key factors in determining the structure of the National Wealth Fund,” he told reporters on the sidelines of a conference in central Moscow.

Russia had stepped up what it calls a de-

“I can say with certainty that the U.S.

The structure of Russia’s international reserves has already changed and the planned changes to the National Wealth Fund will bring its composition closer to that of the central bank’s foreign currency reserves, Kolychev said...

- Source, Reuters, read more here

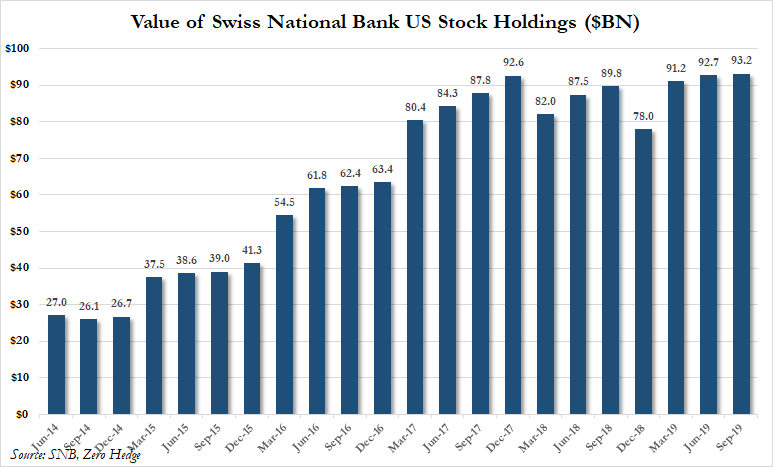

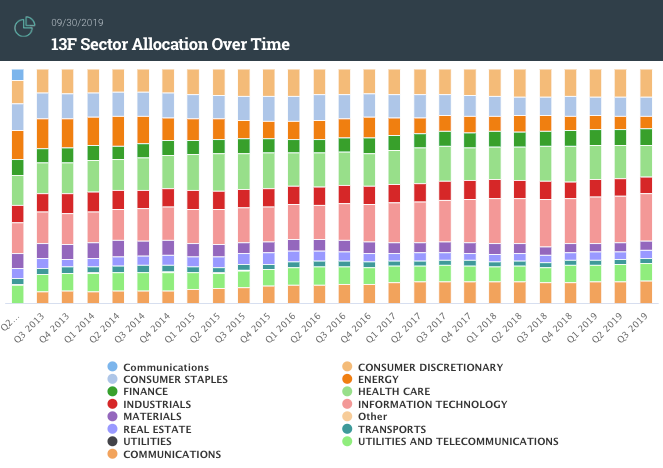

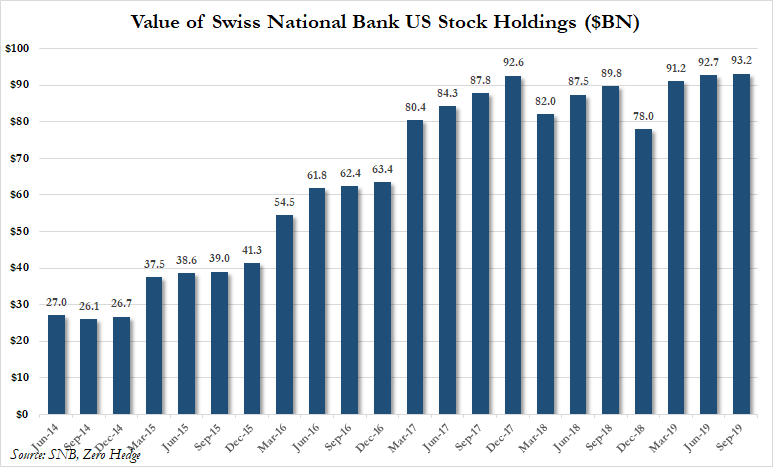

Swiss National Bank Now Owns Record $94 Billion In US Stocks After Q3 Buying Spree

In the third quarter of 2019, one in which the global economy continued to cycle lower , global central banks across the world continued to slash interest rates and launched/expanded quantitative easing programs with very little success at troughing global growth. Still, US equity indices powered to new highs, climbing a wall of worry of President Trump's "trade optimism" tweets.

It seemed quite evident over the quarter that President Trump's tweeting of constant fake trade news and record stock buybacks juiced the market to new highs, however, what was really taking place was the Swiss National Bank (SNB) printing money out of thin air buying stocks with no regard for price or cost.

SNB's motive was to boost market confidence that a 2016-style rebound in the economy was imminent by sending stock indexes to new highs.

The SNB's latest 13F showed total holdings of US stocks have hit a record high, now valued at $94.1 billion, up 1.5% in 3Q.

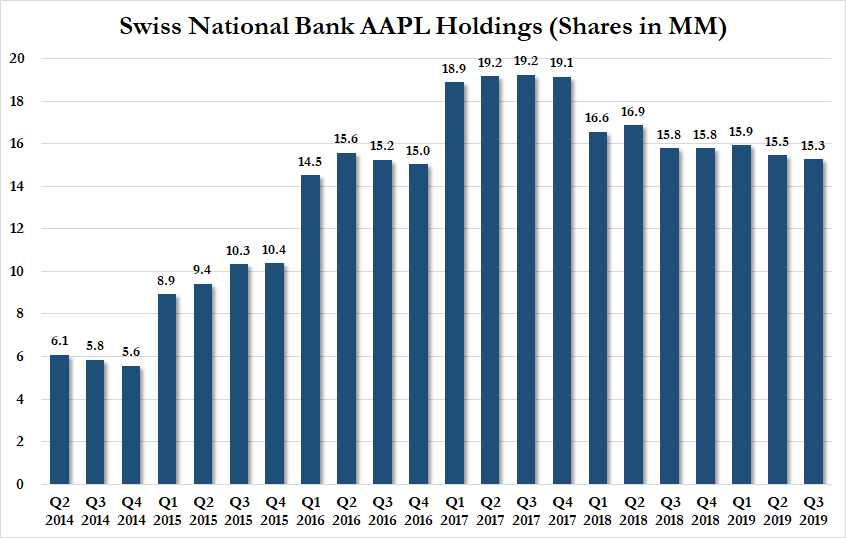

Some notable observations: in the third quarter, after the SNB printed money out of thin air, it then added 1.28 million shares of BABA, 970K shares of FIS, 628K of JD, 537K of JNPR, 472K of GPN, and 257K of MSFT.

Other notable observations: it sold 1.85 million shares of FDC, -301K shares of ORCL, -229K shares of CSCO, and -188K shares of AAPL.

Top holdings continue to be AAPL (3.63% of total portfolio), MSFT (3.58% of total portfolio), AMZN (2.55% of total portfolio), FB (1.50% of total portfolio), and GOOG (1.34% of total portfolio).

SNB's asset allocation over the last six years has been heavyweight technology, healthcare, and consumer discretionary stocks.

SNB printing money out of thin air and buying a handful of stocks that push the broader equity market to new highs, has created an illusion that President Trump's "trade optimism" could lead to a global economic recovery. And when a global recovery doesn't come -- the trade war will be blamed.

It seemed quite evident over the quarter that President Trump's tweeting of constant fake trade news and record stock buybacks juiced the market to new highs, however, what was really taking place was the Swiss National Bank (SNB) printing money out of thin air buying stocks with no regard for price or cost.

SNB's motive was to boost market confidence that a 2016-style rebound in the economy was imminent by sending stock indexes to new highs.

The SNB's latest 13F showed total holdings of US stocks have hit a record high, now valued at $94.1 billion, up 1.5% in 3Q.

Some notable observations: in the third quarter, after the SNB printed money out of thin air, it then added 1.28 million shares of BABA, 970K shares of FIS, 628K of JD, 537K of JNPR, 472K of GPN, and 257K of MSFT.

Other notable observations: it sold 1.85 million shares of FDC, -301K shares of ORCL, -229K shares of CSCO, and -188K shares of AAPL.

Top holdings continue to be AAPL (3.63% of total portfolio), MSFT (3.58% of total portfolio), AMZN (2.55% of total portfolio), FB (1.50% of total portfolio), and GOOG (1.34% of total portfolio).

SNB's asset allocation over the last six years has been heavyweight technology, healthcare, and consumer discretionary stocks.

SNB printing money out of thin air and buying a handful of stocks that push the broader equity market to new highs, has created an illusion that President Trump's "trade optimism" could lead to a global economic recovery. And when a global recovery doesn't come -- the trade war will be blamed.

- Source, Zero Hedge

Tuesday, 12 November 2019

Ron Paul: End of Liberty or End of The Fed, Which Will Come First?

- Source, Ron Paul

Monday, 11 November 2019

Egon Von Greyerz: Hell Will Soon Be Unleashed In Global Markets

“The gold price is determined in a Casino with massive leverage and it has nothing to do with the real price of physical gold. More about that later in the article…

At what point will gold turn from a minority interest, attracting less than 0.5% of world financial assets to a mass-market investment?

Two Decades Ago We Made This Important Decision…

Three decades ago I identified physical gold as the best asset to hold for wealth preservation purposes. Then, almost two decades ago we decided to invest properly in physical gold for ourselves and the investors we advised. Part of our wealth protection plan was obviously to store the gold outside thearea we saw as the biggest risk, namely the financial system. Anyone who stores gold in a bank, ETF or some gold fund has not understood the purpose of physical gold.

Being holders of a minority asset means that 99.5% of the investment population sneers at you and believes you live on a different planet. As a company who passionately wants to help others to protect their wealth, we are fortunate to meet like-minded people. But most of our clients feel very isolated because they have no one to discuss their concerns about the world with.

I would advise anyone with a gold interest to attend a good precious metals conference. In the last two weeks I have been speaking at two excellent gold conferences. One was the Gold Symposium in Sydney and the other one the Edelmetallmesse (International Precious Metals & Commodities Show) in Munich. It is important to pick a conference which includes many participants talking about the risks in the world and who see gold as a remedy against these risks. Many gold conferences are more geared towards gold mining and therefore less interesting for the wealth preservationists.

For anyone who wants confirmation that they are not alone in their analysis of the risks in the world, it is good for the soul to attend one of these gold conferences.

At what point will gold turn from a minority interest, attracting less than 0.5% of world financial assets to a mass-market investment?

Two Decades Ago We Made This Important Decision…

Three decades ago I identified physical gold as the best asset to hold for wealth preservation purposes. Then, almost two decades ago we decided to invest properly in physical gold for ourselves and the investors we advised. Part of our wealth protection plan was obviously to store the gold outside the

Being holders of a minority asset means that 99.5% of the investment population sneers at you and believes you live on a different planet. As a company who passionately wants to help others to protect their wealth, we are fortunate to meet like-minded people. But most of our clients feel very isolated because they have no one to discuss their concerns about the world with.

I would advise anyone with a gold interest to attend a good precious metals conference. In the last two weeks I have been speaking at two excellent gold conferences. One was the Gold Symposium in Sydney and the other one the Edelmetallmesse (International Precious Metals & Commodities Show) in Munich. It is important to pick a conference which includes many participants talking about the risks in the world and who see gold as a remedy against these risks. Many gold conferences are more geared towards gold mining and therefore less interesting for the wealth preservationists.

For anyone who wants confirmation that they are not alone in their analysis of the risks in the world, it is good for the soul to attend one of these gold conferences.

Both the show in Sydney and Munich had a very enthusiastic crowd. For someone who has written newsletters for many years and appeared in interviews, like myself, most people in the audience will know you and want to talk to you. The Australians are more expressive and want to shake your hand and have a photo taken.

The Germans are a bit more shy but also have a lot of questions. Both conferences were very well attended — more than in previous years.

- Source, King World News, read more here

Sunday, 10 November 2019

Saturday, 9 November 2019

Friday, 8 November 2019

G. Edward Griffin: Bankers Are Waiting for the Big Collapse

That is kind of a crude way of putting it, but I think they are going for broke because they know it is broke , and there is not much they can do about it.” So, what’s the plan by the bankers? Griffin says, “I think I know.

They are waiting for the big collapse to come. They will personally be okay because they will have amassed hard assets. They are trying to hold all the gold, all the silver, all the real estate and all the stuff that has value.

They want all the tools, factories and food supplies, but everything else, based on numbers, paper and debt, that will collapse. So, they will be able to pick up everything for pennies on the dollar.”

- Source, USA Watchdog

Thursday, 7 November 2019

Wednesday, 6 November 2019

David McAlvany Explains How to Truly Own Precious Metals

- Source, Jay Taylor Media

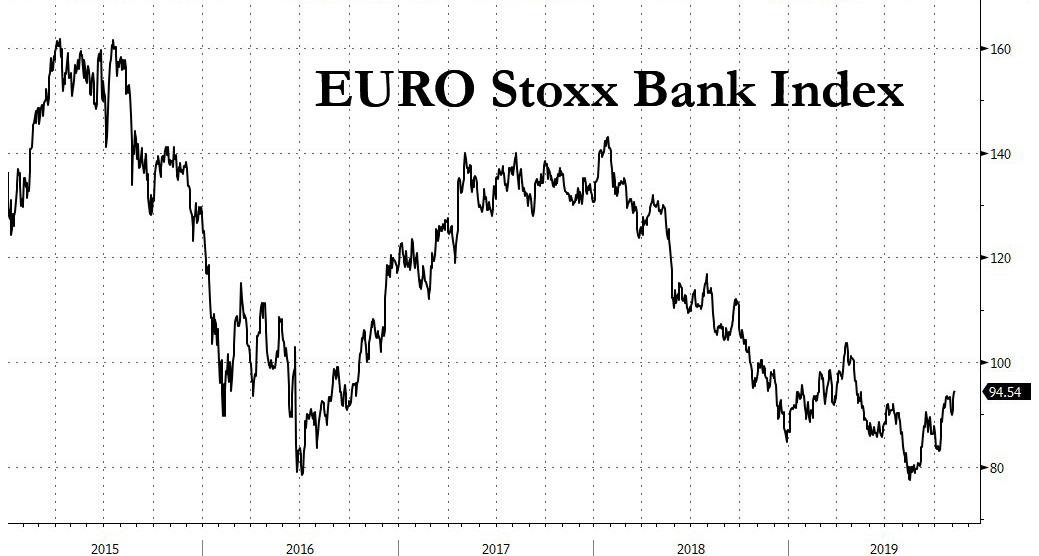

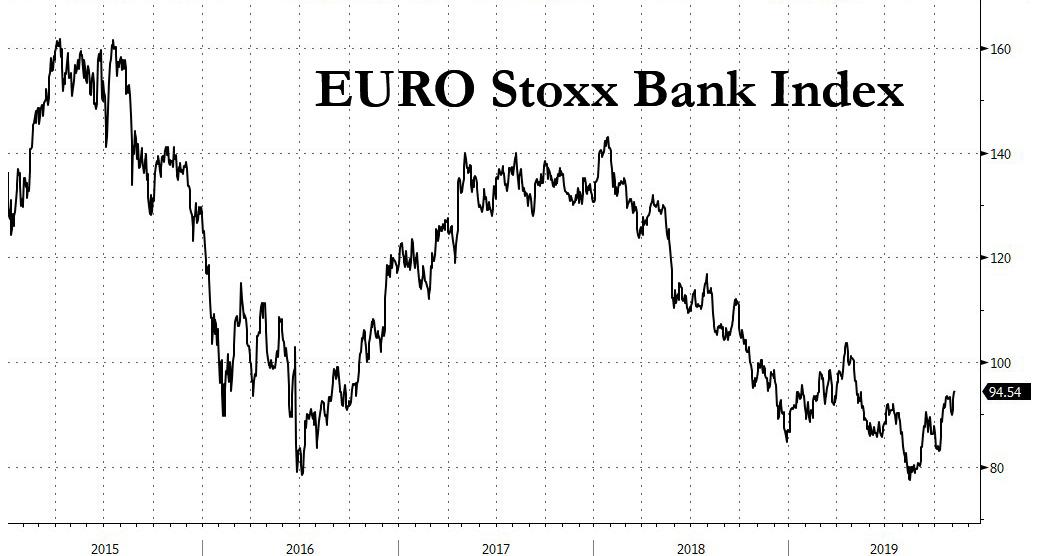

Three Examples Of How Chaos Theory Affects Financial Markets

Chaos Theory – the idea that a butterfly in Thailand could cause a US hurricane – can actually create positive outcomes as well as mayhem. Consider that European banks, German long-term bunds and the offshore yuan are essentially the butterflies making for pleasant investment conditions just now. All have turned sharply in the last 2 months after previous discounting disaster. And all have more room to run.

Chaos Theory gets a bum wrap, and I think the reason is bad branding. The most common explanation of the phenomenon is the classic “a butterfly flapping its wings in Thailand can cause a hurricane in the Gulf of Mexico”. Initial conditions, in other words, can have outsized effects in complex systems like weather patterns. Fair enough, but one usually associates Chaos Theory with bad outcomes like cyclones and stock market crashes.

What about when initial conditions push their way through to create unexpectedly good outcomes? That’sChaos Theory as well, but no one talks about the mayhem created by a lovely day… Bad branding, that, or at least misleading packaging…

Turning to the current sunny spell in global risk markets, three examples of why Chaos Theory can workto investors’ benefit as well as harm.

Exhibit #1: European Bank Stocks:

In early August, the EURO STOXX Banks Index looked like it was about to implode. At 77, it had not been lower since the 1990s. We wrote about it, highlighting that several market bears thought the group was destined to go intochaotic (there’s that word again) free-fall.

But then the group found its footing as Eurozone long-term interest rates bottomed (more on that in a minute).

From August 15th to now, the index is up 20%. Disaster averted, at least for now.

The group’s move has lit a fire under global bank stocks. US large cap Financials are up 12% since mid August. Small caps are +8% and Japanese banks are +14%.

Here is a 5-year chart of the index to give you some historical perspective:

Bottom line: European banks are the Lake Victoria of the current rally in globalfinancials and therefore also the source waters for the ongoing lift in value stocks.

Exhibit #2: German 30-year sovereign bonds:

Since the German government runs a balanced budget, long-termbunds are in perennial short supply relative to US Treasuries.

Along with that, the long duration of German 30-years makes this asset singularly twitchy to market sentiment about Eurozone economic growth.

At the end of August, when US-China trade talks were at their nadir, the market for 30-yearbunds was signaling the real risk of a deep European recession. Yields got as low as -0.27%.

Now, the yield on 30-yearbunds is positive again to the tune of 0.16%. Ok, not great but also not (quite) staring into the abyss. Treasuries have followed along, assuaging concerns created by a previously inverted yield curve.

Here is a 5-year yield chart for this paper:

Bottom line: the lift in long-term German yields since late August was the spark that reignited the global market’s animal spirits in September and October. Europe may be teetering on the edge of recession, but lessening US-China trade tensions may save it from falling into too deep a hole.

Exhibit #3: The offshore yuan/dollar exchange rate:

When the offshore yuan blew through the old “line in the sand” level of 7/$ in early August, you knewmarkets were worried US-China trade talks were sputtering.

These reached their peak in early September, at 7.19/$.

Since then, the yuan has crawled its way back to (almost) 7.0, closing today at 7.03.

Here is a 1-year chart for the offshore yuan:

Bottom line: even if US-China trade talks seem unpredictable, yuan traders are expressing confidence that they remain on the right track. That feeds into global capital markets’ bullish tone just now.

In summary, these are the 3 butterflies of the current global equity rally, each flapping their wings on distantshores but in aggregate creating something productive rather than “chaos”. A look at the chart for each shows they all have room to run. As such, they are the 3 indicators we’ll be watching most closely. For now, however, this is one example of Chaos Theory that is working in investors’ favor.

Chaos Theory gets a bum wrap, and I think the reason is bad branding. The most common explanation of the phenomenon is the classic “a butterfly flapping its wings in Thailand can cause a hurricane in the Gulf of Mexico”. Initial conditions, in other words, can have outsized effects in complex systems like weather patterns. Fair enough, but one usually associates Chaos Theory with bad outcomes like cyclones and stock market crashes.

What about when initial conditions push their way through to create unexpectedly good outcomes? That’s

Turning to the current sunny spell in global risk markets, three examples of why Chaos Theory can work

Exhibit #1: European Bank Stocks:

In early August, the EURO STOXX Banks Index looked like it was about to implode. At 77, it had not been lower since the 1990s. We wrote about it, highlighting that several market bears thought the group was destined to go into

But then the group found its footing as Eurozone long-term interest rates bottomed (more on that in a minute).

From August 15th to now, the index is up 20%. Disaster averted, at least for now.

The group’s move has lit a fire under global bank stocks. US large cap Financials are up 12% since mid August. Small caps are +8% and Japanese banks are +14%.

Here is a 5-year chart of the index to give you some historical perspective:

Bottom line: European banks are the Lake Victoria of the current rally in global

Exhibit #2: German 30-year sovereign bonds:

Since the German government runs a balanced budget, long-term

Along with that, the long duration of German 30-years makes this asset singularly twitchy to market sentiment about Eurozone economic growth.

At the end of August, when US-China trade talks were at their nadir, the market for 30-year

Now, the yield on 30-year

Here is a 5-year yield chart for this paper:

Bottom line: the lift in long-term German yields since late August was the spark that reignited the global market’s animal spirits in September and October. Europe may be teetering on the edge of recession, but lessening US-China trade tensions may save it from falling into too deep a hole.

Exhibit #3: The offshore yuan/dollar exchange rate:

When the offshore yuan blew through the old “line in the sand” level of 7/$ in early August, you knew

These reached their peak in early September, at 7.19/$.

Since then, the yuan has crawled its way back to (almost) 7.0, closing today at 7.03.

Here is a 1-year chart for the offshore yuan:

Bottom line: even if US-China trade talks seem unpredictable, yuan traders are expressing confidence that they remain on the right track. That feeds into global capital markets’ bullish tone just now.

In summary, these are the 3 butterflies of the current global equity rally, each flapping their wings on distant

- Source, Zero Hedge

Tuesday, 5 November 2019

Max Keiser: China secretly hoarding gold and will unleash crypto backed by metal and destroy USD

I can tell you that the cryptocurrency that China’s rolling out will be backed by gold. It’s a two-pronged announcement. Number one, China’s got 20,000 tonnes of gold, number two, we’re rolling out a crypto coin backed by gold, and the dollar is toast,” Keiser told Kitco News.

- Source, Kitco News

Sunday, 3 November 2019

Wealth Accumulation Is Becoming Impossible

We talk a lot about the falling interest rate, the too-low interest rate, the near-zero interest rate, the zero interest rate, and the negative interest rate. Hat Tip to Switzerland, where Credit Suisse is now going to pay depositors -0.85%. That is, if you lend your francs to this bank, they take some of them every year. Almost 1% of them.

A bank deposit comes with a risk. But instead of compensating you for the risk, the bank pays you nothing. So it’s a return-free risk. And worse than that, a negative rate means that you are paying the bank in order to take the risk of lending to them.

Jabberwocky

Lewis Caroll wrote some pretty crazy stories, but even he did not think of something so absurd as this. A vorpal blade that went snicker-snack on the Jabberwock is nothing, compared to a bank that goes snicker-snack on your deposits! Hmm, maybe there is a good analogy here.

A fantasy role-playing game called Dungeons & Dragons has a magic sword called a vorpal sword that is extra likely to cut off your opponent’s head. And a fantasy economics called Keynes & Monestars has a planner called a central bank that is likely to cut off civilization’s head. But we digress.

Someone might retort “well, don’t put your money in a bank! Put it in the stock market.”

Money in the Stock Market

Of course, a bank depositor does not have money (or irredeemable currency, as today) in a bank. He has lent it to the bank. We believe that it’s important to understand these things at a mechanical level.

More to the point, a stockholder does not have money in the stock market. He paid his money to the prior owner of the stock. That person got the money, and may well have spent it. Perhaps on a Vegas binge. Maybe the bartender who unbottled the booze on his bender bought shares…

But as far as the new stockholder is concerned, his money is long gone. He traded it for stock. Why did he do that? Because he expects that someone else will pay him even more money in the future. Why would someone pay him more? Because that guy expects the next guy to pay even more than that. And so on.

As an aside, this would be all good if the shares went up because the company’s earnings went up. In that case, investors should be happy to pay double—because they’re getting double the earnings. Because they would be getting twice the dividend (or more). However, this does not describe our world. We live in a world of falling interest rates.

As interest the rate falls, people pay more for the same dollar of earnings.

Consider a simple case. Suppose Prudence Inverness bought a share of the Dollar Corporation. She paid $10 for it. TDC earns—you guessed it—one dollar per share. This means the earnings yield on her investment is 10%. The CEO, Dave Dahle, sets the dividend at $0.20, so her dividend yield is 2%.

A year passes and TDC earns —still—one dollar per share. Is Prudence any richer?

Next, Spencer Speccalatore else comes along. He bids $20 on the same share in TDC, with the $1 of earnings and $0.20 of dividend . Now is Prudence any richer now?

If she takes Spencer’s $20, then obviously she is $10 richer. However, Spencer is not. Assuming her purchase of the TDC share for $10 was fair value, then Spencer becomes poorer by paying double for the same share that earns the same dollar.

At any rate, Spencer does this because he expects Willie Wild to buy it from him for $40. And Mr. Wild pays $40 because he expects Mark Madenes to pay $80, and so on.

Obviously, there comes a point at which no further buyer is willing to pay more. Then the price crashes. That is when most people would say that the wealth was lost. This article in the Atlantic captures this idea:

“Between February 2000 and February 2002, the NASDAQ lost three-quarters of its value… By late 2000, more than $5 trillion in wealth had been wiped out.”

Conversion of Wealth to Income

We’ve written many times before, that the wealth of the Spencers, Willies, and Marks is converted into the income of the Prudences, the Spencers, and Willies (yes, some of those who converted their wealth into someone else’s income, later receive yet another person’s wealth as their own income).

When wealth is converted to income, much of that income is spent. That is the moment when it is wiped out. The price collapse occurs later. That’s just the accounting catching up to the reality.

This was a bit of a digression, but important enough to be worth the words necessary to describe this process. However, our main focus today is at a different angle.

Where, in this process of bidding up the same share of TDC with the same dollar of earnings and the same twenty cents of dividend, is wealth being accumulated? We mean this from an economy-wide perspective, not merely looking at Prudence, Mark and Willing. They are the lucky ones who bought lower and sold higher. And, in the end, their cumulative gains were matched by the loss of one Mr. Wild.

All during the process of bidding up the shares, wealth is not being accumulated. It is being dissipated. Each selling shareholder has a gain , and spends some of that gain (even if he would not, the tax man takes some of it).

Interest Matters

We write a lot about the need for interest. This is not merely some lament for the poor wage-earner, who many presume to be too dumb and too unsophisticated to invest properly (i.e. buy shares of TDC at ever-higher prices), and who is therefore relegated to the sad fate of depositing his savings in a bank.

Although of course there are many people who don’t buy shares. And they do deserve some sympathy because they are being given a raw deal.

Our point is much broader than this one group. Those who are smart and sophisticated enough to buy shares of TDC, think to use shares as a surrogate for savings. Rising share price is a substitute for interest. And—unless they are Mark Madenes—it may seem to work for them.

However, there is a key difference. Savings is used to finance an increase of production, a profitable business. The interest is paid out of that increase. Rising share price finances nothing of course, and the capital gain of each selling shareholder comes from the next buyer’s capital.

No wealth is accumulated in this process of bidding up asset prices. In fact, it is being de-cumulated.

The Fed and other central banks have waged a War on Interest. They are now victorious. It’s all over, but the mopping up. Positive interest is not coming back to the franc; zero interest will come to the dollar soon enough.

This is why Monetary Metals is obsessed with paying interest on gold.

Supply and Demand

The prices of the metals barely budged this week.

It is interesting to note that this week, more than one central banker felt it necessary to say something about a possible next crisis. And at least one of them said something about gold. We do not place much stock in what these guys say for obvious reasons. Like Elmer Fudd armed with a gun that couldn’t quite hit any target, the central bankers are armed with a theory that couldn’t quite explain an economy.

However, there are certain things they can see—sometimes ahead of most others. One is the stress on the banks. The Swiss Bankers Association says that negative rates are costing them $2 billion a year. Two billion here, two billion there, and pretty soon it adds up.

The banks want an end to negative rates, but as we have written at great length, this is impossible. So right now, they are facing a drain of their capital of two billion a year. The banks are trying to catch up by charging their clients even negativer rates.

This could cause a run on the banks, if depositors withdraw paper bank notes (which have an interest rate of zero). Just like in our discussion of the repo market intervention, each policy imposed by the central banks has consequences that make them impose the next policy. We said:

“An image that comes to mind is a mad ocean monster, like akraken . It is blasting a sea dike with many high-pressure hoses. This causes leaks, but thekraken keeps plugging them with more and more tentacles.”

We eagerly await (not really, just a figture of speech) the next policy response of the Swiss National Bank, and the other central banks. Especially if these rumblings of the next crisis are real. As students of the gold basis, we expect to see an early warning.

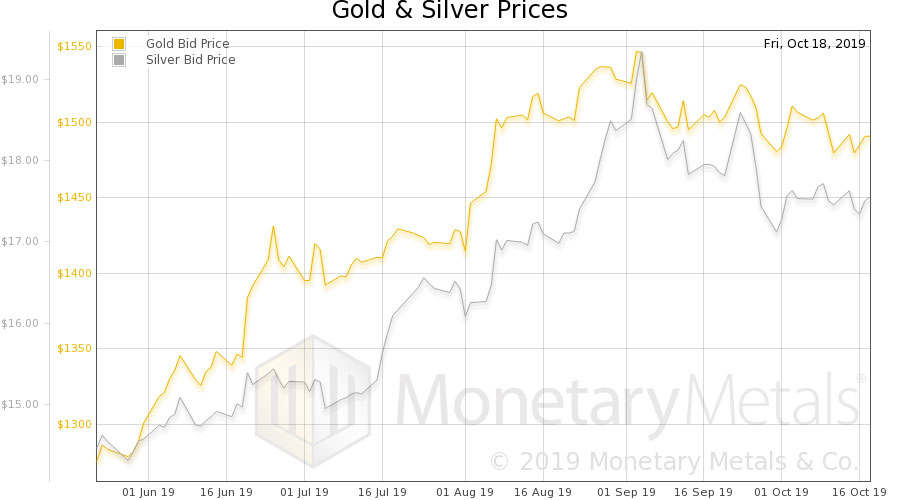

Read on for a look at that early warning system. But, first, here is the chart of the prices of gold and silver.

(Click on images to enlarge)

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio).

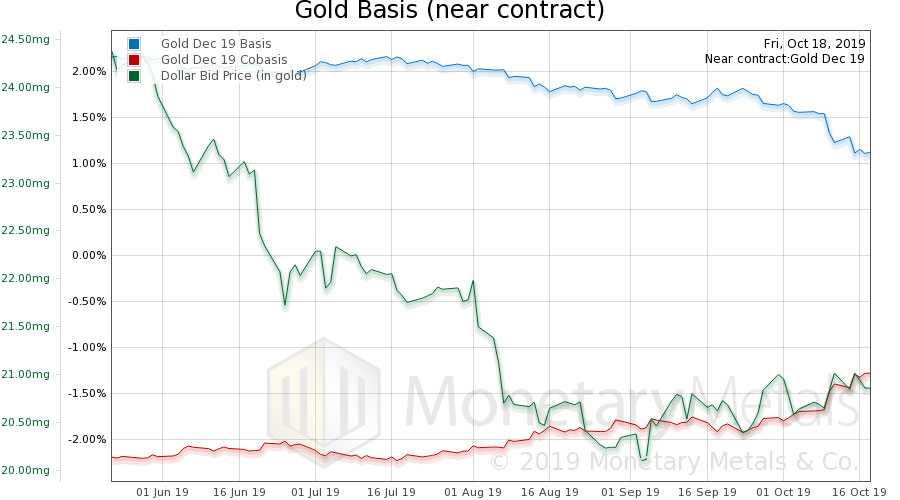

Here is the gold graph showing gold basis, cobasis and the price of the dollar in terms of gold price .

The cobasis increased again, with no drop in price. Gold is just that smidge scarcer that it was. Though we must emphasize this is far from the level we would expect in a crisis.

The Monetary Metals Gold Fundamental Price, was up another $19 this week, to $1,483.

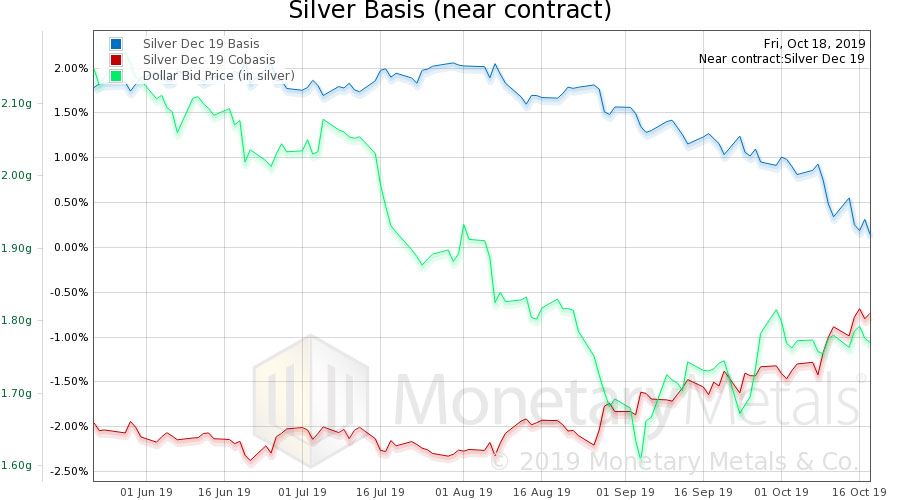

Now let’s look at silver.

In silver, the same thing happened to the (December) cobasis , though not the silver basis continuous.

- Source, Keith Weiner via 321gold

Friday, 1 November 2019

There’s No Silver Shortage…For Now

Now the market is taking a breather, but we could well see the traditional Q4 rally could take prices much higher.

There have been persistent rumors about a coming silver shortage, but David is unconvinced. But that doesn't mean there's not one looming, especially if investment demand picks up.

- Source, Financial Survival Network

Thursday, 31 October 2019

Rob Kirby: Rigged Markets & ZIRP Forcing Us All Into Gambling

With Zero and Negative Interest Rate Policies (ZIRP & NIRP) forcing fund managers, pension managers, and even safety-seeking investors into reckless speculation in the casino of our sinking ship of state.

With each passing day, our dystopic financial Titanic lists further into the deep, and our risk exposure breaches formerly unthinkable crisis levels…

What is a person to do, to retain their bearings, to regain solid footing, and to secure a lifeboat for their loves ones?

- Source, Reluctant Preppers

Wednesday, 30 October 2019

Richard Maybury Describes How Governments Use Propaganda

- Source, Jay Taylor

Tuesday, 29 October 2019

Zuckerberg Defends The "Libra" While Venezuelans Say "Fiat No Mas!"

- Source, Silver Doctors

Monday, 28 October 2019

Ron Paul: The Fed is On its Last Legs & Foreign Central Banks Are Going For Gold

Not only are more and more foreign nations rejecting America's aggressive and militant foreign policy, but they're also ripping themselves away from the The Fed's dollar.

Foreign central banks are increasingly gravitating to sound money like gold. The Fed is on its last legs.

- Source, Ron Paul

Sunday, 27 October 2019

McKinsey: 60% Of Banks May Not Survive the Next Economic Slowdown

A third of banks around the world

- Source, Wall St for Main St

Saturday, 26 October 2019

The gold companies that benefit most from a metals price rally

“It’s the producers, because they’re getting more money for the products they produce. They really see the benefit, and it’s much, much more muted on the juniors. They’re really results driven and if they’re not doing the exploration, they’re not getting results,” Murphy told Kitco News on the sidelines of the 121 Mining Conference in New York.

Friday, 25 October 2019

Craig Hemke: A Financial Crash is Near

So, there is some pretty nasty stuff brewing out there. There is some real liquidity monetary tightness that is pushing things to the verge of collapse, really.

They are doing everything they can to stave it off. The curtain is being pulled back on central bankers, and it reveals them to be charlatans.

They are not these all-knowing masters of the universe looking out for the world. No, they don’t know what they are doing. They are just trying to maintain this illusion.

The demand for all the massive amount of money from the central banks and the Fed leads to a crisis of confidence in their ability to keep things going.

Why would you not want gold and silver? There is a global awakening to that, and that is why prices have hit new all-time highs in 70 currencies around the globe, and we will see new all-time highs in dollar terms, too, next year.”

- Source, USA Watchdog

Thursday, 24 October 2019

Why Gold Investors Will Never Be the Same Again

“I think the majors have changed mindset thinking that it’s not about production profile, it’s about generating free cash flow and maintaining dividends,” Mazumdar told Kitco News on the sidelines of the 121 Mining Investment Conference in New York.

- Source, Kitco News

Wednesday, 23 October 2019

Gold Has Dual Purpose: Portfolio Insurance for Inflation or Deflation

Like other forms of faith, those who believe in gold will not apostatize, and most who do not believe cannot be convinced. That is the generational fallout from some 50 years throughout which the majority of the global population believed that fiat currency was the only legitimate store of value.

On that score, I would hope that gold will eventually be judged on the quality of its track record — its massive liquidity, strong price performance versus fiat currencies, and eventual use as a digital savings asset and payments medium (see The Rebirth of Gold as Money).

My career has involved interacting with many of the most notable investors in the gold sector. Although these gold aficionados all share a similar long-term belief in the advantages of gold, it has never ceased to amaze me how different their macro-economic outlooks are, especially as it relates to the potential for harmful inflation or deflation. Few strategists or economists go into depth about what extreme scenarios could play out for either of these possibilities. Let’s consider both in the context of gold’s utility as an asset.

Gold has successfully been used bysavers as a store of value during periods of high inflation and corresponding currency devaluation. Deflation, on the other hand, triggers debilitating solvency and liquidity issues which usually lead to severe market corrections, again leaving gold as a better asset to own outside of those correlated with credit and equity markets. The reason why gold supporters do not debate their differentiated macro forecasts is that gold is a chameleon that can benefit from both outcomes, and thereby provides insurance from negative market developments stemming from polarized monetary outcomes, as shown in Figure 1.

Figure 1. Gold Provides Proven Portfolio Protection1

This chart measures the performance of Spot Gold versus the S&P 500 Index versus during 11 crisis periods since 1985. Gold returned an average +6.4% compared to -21.7% for the S&P 500 for these 11 crisis periods. Click here to view a larger version of this chart.

My career has involved interacting with many of the most notable investors in the gold sector. Although these gold aficionados all share a similar long-term belief in the advantages of gold, it has never ceased to amaze me how different their macro-economic outlooks are, especially as it relates to the potential for harmful inflation or deflation. Few strategists or economists go into depth about what extreme scenarios could play out for either of these possibilities. Let’s consider both in the context of gold’s utility as an asset.

Gold has successfully been used by

Figure 1. Gold Provides Proven Portfolio Protection1

This chart measures the performance of Spot Gold versus the S&P 500 Index versus during 11 crisis periods since 1985. Gold returned an average +6.4% compared to -21.7% for the S&P 500 for these 11 crisis periods. Click here to view a larger version of this chart.

- Source, Sprott

Tuesday, 22 October 2019

Bob Moriarty: There Is No Rush Like A Gold Rush

Okay, lots of people are smart enough to get in this stuff, BitCon, three bucks, or five bucks, or fifty bucks. They were smart enough to get in, but damn, it goes up to $20,000 and they’re too fucking dumb to bail out. If you refuse to take a profit, you are going to have to take a loss.

Strange thing is, my book, Nobody Knows Anything, should be a New York Times best seller. It is that fucking good. It is simple. Buy things when they’re cheap and sell them when they’re dear. Nobody wants to do that.

If they’re smart enough to buy cheap, they want to wait until it’s gone up 100 fold and then it’s, “Well, if it goes up a little bit more, then I’ll sell.” Investing has nothing to do with management, has nothing to do with commodity. It has nothing to do with the country risks. It has nothing to do with any of that.

It has to do with human behavior. There is no rush like a gold rush. You use the correct term, there is this little tiny door and everybody’s going to try to squeeze through the door at the same time.

Look atWeWork . There’s a company that’s absolutely classic. It’s fraud. There is absolutely nothing of substance there. It’s the dumbest idea that I’ve ever seen. It had a 50 billion dollar market cap in theory a month ago, and now it’s got a 10 billion dollar market cap, and JP Morgan’s about to dump 5 billion dollars into it.

Boy, if they get a cent of that back, I would be amazed.

If they’re smart enough to buy cheap, they want to wait until it’s gone up 100 fold and then it’s, “Well, if it goes up a little bit more, then I’ll sell.” Investing has nothing to do with management, has nothing to do with commodity. It has nothing to do with the country risks. It has nothing to do with any of that.

It has to do with human behavior. There is no rush like a gold rush. You use the correct term, there is this little tiny door and everybody’s going to try to squeeze through the door at the same time.

Look at

Boy, if they get a cent of that back, I would be amazed.

- Source, Energy and Gold, Read More Here

Monday, 21 October 2019

Are we prepared for a shortage of rare earths metals?

“Rare earths are somewhat unique in the sense that China effectively owns the entire supply chain.

I think that in light of the trade war rhetoric going back and forth, which I don’t see any end to any time soon, you’re looking at weaponization of rare earths on the part of China,” Berry told Kitco News on the sidelines of the 121 Mining Conference in New York.

- Source, Kitco News

Subscribe to:

Posts (Atom)