- Source, SRS Rocco Report

Wednesday, 29 July 2020

Massive Change in Silver: We Have Entered Into a New Bull Market

Saturday, 25 July 2020

Dollar Index Falls Below March 2020 Support Levels, Headed Back Down to 2018 Lows?

- Source, Wall St for Main St

Friday, 24 July 2020

Michael Pento: Get Ready for Stagflation and the Greater Depression

You can make an argument that the Fed can fight deflation because it can continue to prop up asset prices. That’s true, and it’s a proven fact, but what does the Fed do when inflation starts to run intractable?

When inflation becomes the problem, what can the Fed do? Promise to buy stocks and print more money? What can the Fed do? Print money to buy down interest rates when the economy is in full revolt?

When money managers are shorting bonds and driving yields to the moon. No, the only thing they can do is stop printing money and promise to fight inflation.

That’s when you are going to get 6,000 on the Dow Jones Industrial average because there’s nothing they can do.

The Fed will be rendered impotent.” Pento suggests that people “get out of all financial products with an adjustable interest rate” and lock in at historically low fixed rates.

In closing, Pento says, “This is the best environment for gold I have ever seen in my career. This is in an environment where debt and deficits are surging.

So, debt is exploding, and what does gold like? It likes falling real interest rates. It likes exploding debt, and a little ticker on that is a dollar that’s weakening. That’s why I really like gold.”

- Source, USA Watchdog

Tuesday, 21 July 2020

Chris Martenson: The Mainstream Media Has Blood on Their Hands

Martenson contends the MSM misinformed people, and ‘people died.’” Martenson also says, “People should tune your body up so your body can fight off Covid 19.

You want your body to be as healthy as it can be from an immunological standpoint.” Martenson says the three things you need to take to help fight off Covid 19 are Vitamin D, Zinc and Quercetin. Martenson says the good news is Covid 19 is definitely going to “trend down by the end of the year.”

- Source, USA Watchdog

Monday, 20 July 2020

Liberty & Finance: Think Your Not Lending Money to Insolvent Banks? Think Again

Although governments officials state that “all is well, nothing to see here, savings are protected,” the actual laws do not protect the ordinary saver, but the banks.

Economist and public-interest advocate John Adams, co- host of “In the Interest of the People,” returns to Liberty and Finance / Reluctant Preppers to expose the dirty little secret trap that’s ready to spring on unsuspecting savers, and to announce his proposed amendment to close this loophole in Australia, which he has submitted to the Australian Parliament inquiry.

- Source, Reluctant Preppers

Sunday, 19 July 2020

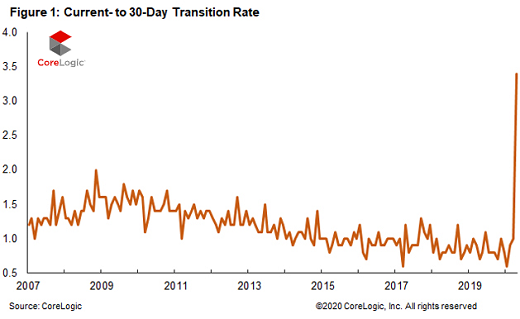

It Starts: Mortgage Delinquencies Suddenly Soar at Record Pace

OK, it’s actually worse. Mortgages that are in forbearance and have not missed a payment before going into forbearance don’t count as delinquent. They’re reported as “current.” And 8.2% of all mortgages in the US – or 4.1 million loans – are currently in forbearance, according to the Mortgage Bankers Association. But if they did not miss a payment before entering forbearance, they don’t count in the suddenly spiking delinquency data.

The onslaught of delinquencies came suddenly in April, according to CoreLogic, a property data and analytics company (owner of the Case-Shiller Home Price Index), which released its monthly Loan Performance Insights today. And it came after 27 months in a row of declining delinquency rates. These delinquency rates move in stages – and the early stages are now getting hit:

Transition from “Current” to 30-days past due: In April, the share of all mortgages that were past due, but less than 30 days, soared to 3.4% of all mortgages, the highest in the data going back to 1999. This was up from 0.7% in April last year. During the Housing Bust, this rate peaked in November 2008 at 2% (chart via CoreLogic):

From 30 to 59 days past due: The rate of these early delinquencies soared to 4.2% of all mortgages, the highest in the data going back to 1999. This was up from 1.7% in April last year.

From 60 to 89 days past due: As of April, this stage had not yet been impacted, with the rate remaining relatively low at 0.7% (up from 0.6% in April last year). This stage will jump in the report to be released a month from now when today’s 30-to-59-day delinquencies, that haven’t been cured by then, move into this stage.

Serious delinquencies, 90 days or more past due, including loans in foreclosure: As of April, this stage had not been impacted, and the rate ticked down to 1.2% (from 1.3% in April a year ago). We should see the rate rise in two months and further out.

Overall delinquency rate, 30-plus days, jumped to 6.1%, up from 3.6% in April last year. This was the highest overall delinquency rate since January 2016 (on the way down).

These delinquency rates are the first real impact seen on the housing market by the worst employment crisis in a lifetime, with over 32 million people claiming state or federal unemployment benefits. There is no way – despite rumors to the contrary – that a housing market sails unscathed through that kind of employment crisis...

The onslaught of delinquencies came suddenly in April, according to CoreLogic, a property data and analytics company (owner of the Case-Shiller Home Price Index), which released its monthly Loan Performance Insights today. And it came after 27 months in a row of declining delinquency rates. These delinquency rates move in stages – and the early stages are now getting hit:

Transition from “Current” to 30-days past due: In April, the share of all mortgages that were past due, but less than 30 days, soared to 3.4% of all mortgages, the highest in the data going back to 1999. This was up from 0.7% in April last year. During the Housing Bust, this rate peaked in November 2008 at 2% (chart via CoreLogic):

From 30 to 59 days past due: The rate of these early delinquencies soared to 4.2% of all mortgages, the highest in the data going back to 1999. This was up from 1.7% in April last year.

From 60 to 89 days past due: As of April, this stage had not yet been impacted, with the rate remaining relatively low at 0.7% (up from 0.6% in April last year). This stage will jump in the report to be released a month from now when today’s 30-to-59-day delinquencies, that haven’t been cured by then, move into this stage.

Serious delinquencies, 90 days or more past due, including loans in foreclosure: As of April, this stage had not been impacted, and the rate ticked down to 1.2% (from 1.3% in April a year ago). We should see the rate rise in two months and further out.

Overall delinquency rate, 30-plus days, jumped to 6.1%, up from 3.6% in April last year. This was the highest overall delinquency rate since January 2016 (on the way down).

These delinquency rates are the first real impact seen on the housing market by the worst employment crisis in a lifetime, with over 32 million people claiming state or federal unemployment benefits. There is no way – despite rumors to the contrary – that a housing market sails unscathed through that kind of employment crisis...

- Source, Wolf Street Report, read more here

Friday, 17 July 2020

A Second Wave of Panic Buying is Here, Supply Chain Breaking Down

In places like Hong Kong, we're seeing a second wave of panic buying whereas places like Australia are starting to already die down. But there's more to the story than meets the eye.

As we see a second wave of lockdowns in many places throughout the world, the fear is leading to many people panic buying goods. One would certainly think the supply chain would learn from the previous catastrophe, but it hasn't.

Or perhaps, they're utilizing fear to mark up prices and make more money which is the most logical explanation considering Mexico had little to no actual panic buying despite goods and services internationally being more difficult to come upon.

- Source, World Alternative Media

Thursday, 16 July 2020

Tuesday, 14 July 2020

Craig Hemke: When Shorting Stops, Silver Pops

What about silver? Why is it lagging behind gold? It takes nearly 100 ounces of silver to equal 1 ounce of gold.

That ratio is going to start coming down dramatically. Financial writer and precious metals expert Craig Hemke explains why, “JP Morgan has been accumulating all this silver and shorting against it as a hedge, managing the price and monopolistically controlling it.

- Source, USA Watchdog

Sunday, 12 July 2020

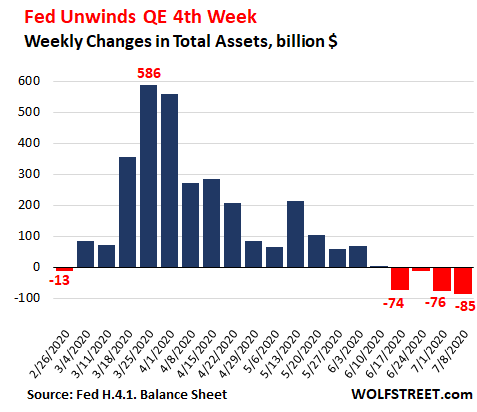

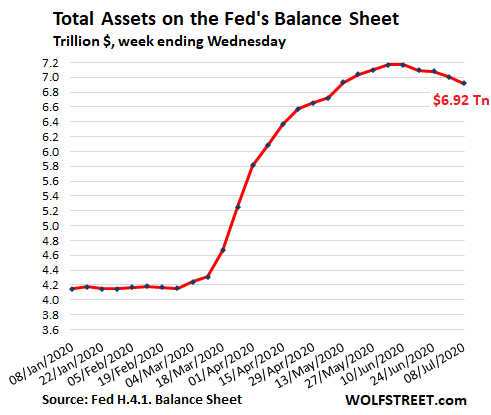

QE Unwind Speeds Up: Fed’s Assets Drop $85 Billion, Four-Week Total -$248 Billion

OK, this balance-sheet shrinkage, now in its fourth week, is going faster than I’d expected. Total assets on the Fed’s balance sheet for the week ended July 8, released this afternoon, dropped by -$85 billion, the fourth week in a row of declines. This brought the four-week total drop to -$248 billion:

Back on April 9, when markets were just emerging from chaos after the Fed had thrown $1.5 trillion at them in the span of four weeks, Fed Chair Jerome Powell said in a webinar at Brookings that “when private markets are once again able to perform their vital functions of channeling credit and supporting economic growth, we will put these emergency tools away.”

This matched what he and other Fed officials had said in the year or so before the Crisis, that at the “next crisis,” they would throw all the Fed’s might at the problem up front, and then they’d back off, rather than let QE drag on for years. And they did.

By peak-QE in early June, the Fed had increased its assets by $2.86 trillion. It has since then whittled this increase down by $248 billion. Note the systematic front-loading then tapering the asset purchases and letting assets top out at $7.16 trillion, and then letting them decline, now down to $6.92 trillion:

Assets by category.

Repo balances dropped by $34 billion, to just $41 billion, the lowest since the Fed starting ramping up repos. Repurchase agreements are on the way out. There were zero overnight repos on the balance sheet, and only some older term repos that hadn’t unwound yet.

The Fed made repos less attractive over time. On June 16, it raised the bid rate, and for market participants there are now better deals available in the repo market. The Fed is still offering theoretically huge amounts of repurchase agreements every day, but there are no longer any takers...

Back on April 9, when markets were just emerging from chaos after the Fed had thrown $1.5 trillion at them in the span of four weeks, Fed Chair Jerome Powell said in a webinar at Brookings that “when private markets are once again able to perform their vital functions of channeling credit and supporting economic growth, we will put these emergency tools away.”

This matched what he and other Fed officials had said in the year or so before the Crisis, that at the “next crisis,” they would throw all the Fed’s might at the problem up front, and then they’d back off, rather than let QE drag on for years. And they did.

By peak-QE in early June, the Fed had increased its assets by $2.86 trillion. It has since then whittled this increase down by $248 billion. Note the systematic front-loading then tapering the asset purchases and letting assets top out at $7.16 trillion, and then letting them decline, now down to $6.92 trillion:

Repo balances dropped by $34 billion, to just $41 billion, the lowest since the Fed starting ramping up repos. Repurchase agreements are on the way out. There were zero overnight repos on the balance sheet, and only some older term repos that hadn’t unwound yet.

The Fed made repos less attractive over time. On June 16, it raised the bid rate, and for market participants there are now better deals available in the repo market. The Fed is still offering theoretically huge amounts of repurchase agreements every day, but there are no longer any takers...

- Source, Wolf Street Report, read more here

Friday, 10 July 2020

Rob Kirby: Price Inflation and Shortages Have Begun

Rob Kirby stopped by Silver Doctors on July 7th, 2020, for a robust discussion on the economy and the markets, with special focus on gold, silver, the US dollar, the unsustainable debt, and what Rob sees coming down the pike.

- Source, Silver Doctors

Thursday, 9 July 2020

Real Vision: How the 2008 Financial Crisis Still Impacts the Present

- Source, Real Vision

Monday, 6 July 2020

Friday, 3 July 2020

Liberty Finance: Big Changes Are Coming for Gold Holders

E.B. Tucker, author of the new book, “Why Gold? Why Now? The War Against Your Wealth and How to Win It,” returns to Liberty and Finance / Reluctant Preppers to answer viewers’ questions on the present & future role gold in our lives, and what drastic changes are likely coming that we should be aware of and prepared for to survive and thrive in the times ahead!

- Source, Liberty and Finance

Wednesday, 1 July 2020

Golden Rule Radio: Gold Holds Strong As Industrial Metals Soften

Gold touched 8 year highs as the usual trend of summer seasonal pricing movements are called into question. A spike in new virus cases has rattled equities slightly, will this propel the metals higher as uncertainty looms once again over the equities sector?

- Source, Golden Rule Radio

Subscribe to:

Comments (Atom)