Gold prices held steady on Friday after rising above $1,280 in the previous session as weak U.S. data pushed the dollar off 2-year highs and reignited hopes of a rate cut by the Federal Reserve this year.

Spot gold was steady at $1,283.21 per ounce by 0653 GMT, after rising as much as 1.1% to a one-week peak of 1,287.23 in the previous session. The metal has risen 0.5% so far this week.

U.S. gold futures for June were down 0.2% at 1,283.10.

“Gold has found a very good support around $1,270. There was some short covering after the (weak U.S.) data that pushed prices up. However, the upside could be limited as $1,290 is acting as a strong resistance,” said Peter Fung, head of dealing at Wing Fung Precious Metals.

The U.S. dollar retreated after hitting its highest level in two years as weak domestic data and the potential economic fallout from the trade war with China increased expectations for an interest-rate cut this year.

Sales of new U.S. single-family homes fell from near an 11-1/2-year high in April as prices rebounded and manufacturing activity hit its lowest level in almost a decade in May, suggesting a sharp slowdown in economic growth was underway.

While the expectations of a rate cut is good for gold, prices can go higher only if the metal can break above $1,290-$1,300 range with the dollar still being strong, Fung added.

Lower interest rates tend to lift gold as it reduces the opportunity cost of holding the non-yielding bullion.

Four Fed officials on Thursday conceded that aggravating U.S.-China tensions could threaten economic growth, a marked deviation from Chair Jerome Powell’s Monday comments where he said it was too early to ascertain the impact of trade on the trajectory of monetary policy.

However, gold has been under pressure of late as investors preferred the U.S. dollar amid intensifying U.S.-China trade tensions. The bullion is down nearly 5 percent since touching a 10-month peak in February at $1,346.73.

“Gold has disappointed to the upside often in the past and we would therefore like to see a string of more consistent gains before we feel comfortable signalling an all-clear on the upside,” INTL FCStone analyst Edward Meir said in a note.

Spot gold may break a resistance at $1,286 per ounce and edge up to the next resistance at $1,290, according to Reuters technical analyst Wang Tao...

Markets are a mess. Across the world and across asset classes, there were new highs and lows Thursday, and sharp deviations from trends. Something is definitely up. But what?

There is also, of course, a welter of news coverage of the increasing hostilities between China and the U.S. over trade and technology. Does it therefore follow that the trade war is to blame for the turbulence in markets? We should not take this for granted.

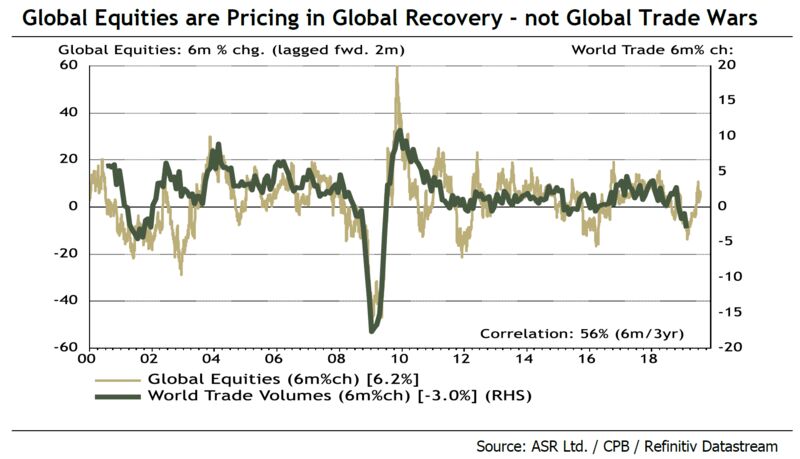

So, could this be about world trade? Equity traders do not generally think of world trade data much in their day-to-day work, but it turns out that changes in equities do tend to predict changes in global trade volumes. The following chart, from London’s Absolute Strategy Research, shows that equity market moves tend to move ahead of changes in trade flows, with a six-month lag:

The issue here is that the rebound in world equities since the Christmas Eve selloff suggests that traders are pricing in a trade recovery. This would imply that they are due quite a correction. Further, trade volumes appear to be enduring the most significant interruption yet to their steady improvement since the aftermath of Lehman’s bankruptcy:

A further argument that this market selloff, unlike the one that preceded it in December, is about trade, might come from the relative performance of emerging markets. Rightly or wrongly, they are seen as far more exposed to trade conflict than the U.S. This might explain why the sell-off at the end of last year functioned as a correction to drawn-out U.S. outperformance, while this latest moment has seen emerging markets lag behind the S&P 500 even more. At this point, all the outperformance by emerging markets since 2003 has been canceled out – an extraordinary statistic given the speed of growth in much of the emerging world.

But despite this, it is hard to say that what’s going on is just about trade. Or at least, if the trade conflict is driving this it is leading to a startling and swift reappraisal of the prospects for the economy.

The recent rise in the price of oil has gone into a sudden reverse, for reasons that can mostly be explained with reference to demand and supply (or an excess of it) in the oil market. That is an important driving factor in its own right, and tends to reduce inflation forecasts in the bond market. That said, the way breakeven rate on Treasuries have dropped in the last few weeks is startling and goes far beyond a normal reaction to a drop in oil prices:

Bear in mind also that tariffs are directly inflationary. All else equal, they increase the prices that Americans have to pay for imported goods. So this move lower in inflation expectations needs more than the trade conflict to explain it.

Meanwhile, Wednesday’s release of the minutes to the Federal Reserve’s last meeting on monetary policy suggested that the central bank was more hawkish than had been thought. In other words, the Fed is keener to keep rates higher for longer than anticipated. The response in the federal funds futures market has been to move the odds of a rate cut this year above 80% for the first time...

Gold prices have been trading range-bound and whether or not prices break out depend mainly on how long the trade war with China lasts, this according to Phil Streible, senior market strategist of RJO Futures.

“I think that if we resolve [the trade agreement] at the next meeting, we could see interest rates start to actually poke back up again, the U.S. economy could get heated up again, and we might have this hawkish tone, but if we have it dragged out over a period of well over another year, we could see that really wane on the economy and that’s where your interest rate cuts come in,” Streible told Kitco News.

The gold-silver ratio tested 89 recently, the highest level since 1993, as silver still fails to show signs of life, but this may be a good opportunity to buy the metal, said Bill Baruch, president of Blue Line Futures.

Spot silver closed at $14.41 an ounce on Wednesday, having stayed relatively flat during the trading session. “I think there’s going to be a lot of value down here.

We could see $14 [an ounce], it’s an eyelash away basically, given some of the moves we’ve seen over the last year, but be ready to buy down there.

I think there’s a couple of ways to look at it, and right now, if it doesn’t get to $14, a nice way to get some exposure is to look at selling $14 puts,” Baruch told Kitco News.

A decade ago I pointed out that public pension funds were $2 trillion underfunded and getting worse. More than one person told me that couldn’t be right.

They were correct: It was actually much worse. It has gotten to $2 trillion and much worse in just a few years.

Note that we are talking here about a specific kind of pension: defined benefit plans. They are usually sponsored by state and local governments, labor unions, and a number of private businesses.

Many sponsors haven’t set aside the assets needed to pay the benefits they’ve promised to current and future retirees. They can delay the inevitable for a long time but not forever. And “forever” is just around the corner.

The numbers are large enough to make this a problem for everyone, even those without affected pensions. The underfunded pensions could also be one of the triggers to the unprecedented credit crisis I see coming in the next five years.

The problem is “solvable”… but the solutions will be problems in themselves.

A defined benefit pension plan knows it owes a certain number of retirees certain monthly benefits for life. Their lifespans are quite predictable when the pool is large enough.

From that, it’s simple math to calculate how much money the plan should have right now in order to pay those benefits when they are due. But then the assumptions start.

The plan must presume a future rate of return on the invested portfolio, an inflation rate, and in some cases future health care costs (medical benefits are part of many plans).

So, when we say a plan is “fully funded,” it may not be so if the assumptions are wrong.

Almost all public pension funds assume investment returns somewhere around 7% (and some as high as 8%+). That’s highly unlikely due to the debt we’ve accumulated, and debt is a drag on future growth.

If you make more realistic assumptions on future returns the unfunded liability becomes $6 trillion according to the American Legislative Exchange Council.

A more conservative and realistic approach would force the state and local governments to fund those pension plans at a much higher level. They have only two ways to do that: either raise taxes or reduce services.

That may be the reason policymakers have turned a blind eye to this...

Broadly speaking, banks operate under the concept of maturity transformation. Banks take short-term – less than one year – financing vehicles, such as customer deposits, and use that to finance long-term – more than one year – returns. These returns range from the most commonly understood loans, such as auto loans and mortgages, to investments in equity, bonds and public debt. Banks make money on the interest spread between what they pay to the owners of the money and what is earned from the operations. Banks also make money on other services, such as wealth management and account fees, though these are relatively small compared to the maturity transformation business.

In terms of assets, the primary asset a bank holds is the demand deposit, also referred to as the core deposit. These are your everyday savings and checking accounts. Banks also sell Wholesale Deposits, such as CDs, have shareholder equity and also can take out debt, such as interbank lending. As these assets are owned by someone else, each of them demands a return for the use of those assets. These are part of the costs of operation for a bank. There are also more fixed operating costs, such as employees, buildings and equipment that must also be financed.

So, a bank will take assets and formulate loans on them. Like most of the world, the US operates on a fractional reserve system, one where banks originate loans in excess of the deposits on-hand. Take a look at the balance sheet of a large regional bank, 5/3 Bank, for example. For the 2018 fiscal year, 5/3 reported non-capital assets of $94 billion and a deposit base of $108 billion. However, the cash and cash equivalent component of these assets stood at $4.4 billion, or just 4% of demand deposits. It is critical, then, that the bank convinces those depositors to keep their deposits with 5/3 and not request a withdrawal. Doing so would collapse the bank as it's unable to quickly make good on any withdrawal request greater than 4% of the deposit base. To do this, the bank pays the depositor interest on the deposit.

How the Collapse Happens

This is where interest stability becomes a problem. When the Federal Reserve manipulates interest rates, banks are able to project fairly steady expenses for operations. While a business likes it when operational costs are relatively constant, this creates major problems for the banking system. When interest rates are suppressed to near 0% for, let’s say, a decade, the banking system builds up an income portfolio that is anchored to that near 0% cost of money. Back to the 5/3 balance sheet, we notice that the bank’s returns were $5.1 billion, or around a 5% average return on assets. $4 billion of those returns are tied up in $94 billion in long term lending. Interest expenses came in at $1 billion, or a little over 1%. The company also has $3.9 billion in relatively fixed operating expenses.

Basically, 5/3 Bank is operating on fairly thin profit margins relative to the bank’s asset base, which makes the bank highly vulnerable to any interest rate fluctuations.

Let’s say the Federal Reserve, then, begins to step up the target interest rate. As the Fed reduces competition on the market and sells assets, interest rates rise as these new assets begin to compete with existing assets. 5/3 then runs into a problem. If the risk-free rate starts to rise, depositors will look at that paltry deposit return and begin to wonder why they’re keeping money in the bank when other low risk vehicles are now offering higher returns. Since 5/3 can’t afford to lose much cash, the bank will be prompted to start raising deposit rates since they want to keep money in the bank. They will also have to refinance short term revolving debt at a higher rate.

The quandary to the bank is that nearly their entire revenue stream is made up of fixed-return vehicles. The effective spread between total costs and total revenue is just 0.2% of assets. This means that if financing costs increase by more than 20 basis points, 5/3 bank begins to take a loss. Since the bank had made loans for over a decade with these extremely low rates in mind, it will take some time to rebuild a portfolio of higher interest rate loans and investments to counterbalance this loss or the bank will seek to engage in high risk investments.

For a normal company, this isn’t a big deal. Companies can withstand losses for periods of time because they tend to build up a cash base to get through weak periods as they retool their operations. A bank, though, lacks this flexibility as they have to retain cash ratios to facilitate depositor withdrawals. A mere 1% increase in total borrowing costs to 5/3 will see the bank run out of cash in just four years, but since the bank has to maintain ratios, this will prompt the bank to begin selling assets to take on additional loans.

The problem compounds two-fold from this point for 5/3. First, the primary assets are income generating, so for every asset sold to keep cash ratios afloat just exacerbates the cash bleed and any new debt has interest expenses that need servicing, servicing without a corresponding asset return. Second, the assets have rates below market rate, so have to be sold at a discount.

Compounding further, every bank is operating like this. Every bank is operating on thin margins that assume a perpetual near-zero rate regime. If one bank has to unload assets to keep cash ratios intact, all the banks are inevitably doing the same. The largest portfolio item is usually the one that attempts liquidation – in 2007 that was the home mortgage. This selloff is self-reinforcing and creates a collapse since there aren’t many entities out there with free cash available to absorb this mass sell-off. Hence why the second largest asset class sitting in the Federal Reserve today is pre-2008 non-performing mortgage backed securities – the MBS holders, banks themselves, were stuck holding the bag. Banks ran to the last entity with cash available — the one that prints it — for a bailout.

Central banks will inevitably respond by trying to stabilize rates again, generally suppressing rates below the last cycle’s floor. Central banks, then, perpetually ratchet the rates down until they run into that 0% barrier then begin to engage in radical monetary policy when that lever is no longer available to pull. Canada’s pattern since 1980 is a perfect example of this, an ever downward sloping roller coaster.

How to Avoid This

If banks didn’t operate in a world of constant interest rates, an increase in rates wouldn’t be an especially large problem. First, if rates are fluctuating, banks naturally hedge against changes in interest rates. When they originate rates at a higher level and rates decline, they will enjoy a higher average return to build a buffer for when rates rise again. Second, if rates engage in natural fluctuation, banks would be hesitant to finance long-term loans using short term vehicles. Fractional reserve banking partially operates on the expectation that interest rates will remain stable for the long run. If the cost of money next month could be 20 basis points higher than it is this month, banks will have incentives to seek fixed financing solutions as opposed to leveraging depositor money. In other words, banks would likely cease engaging in maturity transformation since the risk of interest rates exceeding the return on the entire portfolio is just too high. That or at least limit exposure to this form of lending to something less than a gaudy 27-1 leverage ratio and promote sales of fixed financing like CDs. Market uncertainty and the removal of a central banking backstop would create a more stable banking system, which means naturally moving toward a full-reserve system.

The Federal Reserve, by manipulating interest rates and creating money out-of-thin air, produces economic bubbles that must always end in painful economic busts.

Have you ever noticed that Fed officials never actually acknowledge any of this? They never warn Americans ahead of time and everyone acts surprised when it all comes down.

Today's guest, David Moadel, joins us to share his thoughts on the financial markets, the United States - China trade war and the importance of thinking about alternative approaches to investing.

"The White House is considering conservative economist Judy Shelton to fill one of the two vacancies on the Federal Reserve Board of Governors that President Donald Trump has struggled to fill.

She’s currently U.S. executive director for the European Bank for Reconstruction and Development, and previously worked for the Sound Money Project, which was founded to promote awareness about monetary stability and financial privacy."

"Since President Trump announced his intention to nominate Herman Cain and Stephen Moore to serve on the Federal Reserve’s board of governors, mainstream commentators have made a point of dismissing anyone sympathetic to a gold standard as crankish or unqualified.

But it is wholly legitimate, and entirely prudent, to question the infallibility of the Federal Reserve in calibrating the money supply to the needs of the economy. No other government institution had more influence over the creation of money and credit in the lead-up to the devastating 2008 global meltdown. And the Fed’s response to the meltdown may have exacerbated the damage by lowering the incentive for banks to fund private-sector growth.

What began as an emergency decision in the wake of the financial crisis to pay interest to commercial banks on excess reserves has become the Fed’s main mechanism for conducting monetary policy. To raise interest rates, the Fed increases the rate it pays banks to keep their $1.5 trillion in excess reserves—eight times what is required—parked in accounts at Federal Reserve district banks. Rewarding banks for holding excess reserves in sterile depository accounts at the Fed rather than making loans to the public does not help create business or spur job creation.

Meanwhile, for all the talk of a “rules-based” system for international trade, there are no rules when it comes to ensuring a level monetary playing field. The classical gold standard established an international benchmark for currency values, consistent with free-trade principles. Today’s arrangements permit governments to manipulate their currencies to gain an export advantage.

Money is meant to serve as a reliable unit of account and store of value across borders and through time. It’s entirely reasonable to ask whether this might be better assured by linking the supply of money and credit to gold or some other reference point as opposed to relying on the judgment of a dozen or so monetary officials meeting eight times a year to set interest rates. A linked system could allow currency convertibility by individuals (as under a gold standard) or foreign central banks (as under Bretton Woods). Either way, it could redress inflationary pressures."

I just ordered the book to have a better idea where she is coming from.

Regardless, I am certain she would have been a better choice for Fed chair than Powell, Bernanke, Yellen, or Greenspan.

Bubbles of Increasing Amplitude

Shelton concluded "Central bankers, and their defenders, have proven less than omniscient."

Indeed.

The judgement of the Fed has produced three consecutive bubbles, each bigger than the one before it. The only reason the latest bubble is not acknowledged yet is that it hasn't yet burst.

It's not clear precisely what Shelton has in mind but at least she is headed in the right direction. What's clear is Trump is fighting the wrong battle when it comes to trade.

Tariffs will not fix the alleged problems of currency manipulation. A gold standard would.

Trillions of dollars in Pentagon spending have just disappeared into thin air. The Pentagon failed its first ever audit last year. There is so much off-the-books spending that no one has a clue where it's going. US troops show up in Niger and Congress has no idea how they got there. Is the Pentagon and the military-industrial complex a government unto itself?

Tony Greer, founder of TG Macro, sits down with Jared Dillian, author of a market newsletter called “The Daily Dirtnap.” Greer and Dillian discuss monetary policy, portfolio construction and the dirty little secret your broker won’t tell you. Dillian also sheds light on his shifting focus from institutions to retail investors.

According to a new Washington Post article, President Trump is frustrated with his national security advisor, John Bolton for promising the Venezuela regime change would be a cakewalk.

He's concerned about being boxed into a corner, says an anonymous source. We know the president loves Fox... but is he also watching the Liberty Report?

What will knock this market back to reality? Money manager Michael Pento says, “You will eventually get a recession or eventually you will get inflation.

You might just get both. You might just get a huge case of stagflation to hit this country and around the world. That’s what I am most afraid of.” In closing, Pento warns, “Japan has no growth. There is no growth in Germany.

There is no growth in Italy. We have an earnings recession here in the United States. So, what you have engendered here is most likely a protracted period of stagflation, which is going to lead to an epic and massive crash in asset prices. That’s what you have at your feet, so be careful.”

If rate cuts don’t happen soon, is the economy going to tank? Economist John Williams says, “The economy is tanking, and I’ll contend it already has, although we have not seen it in the GDP reporting.

The ultimate thing here is you have a collapse in the dollar. I am talking about a hyperinflationary collapse.

Your purchasing power becomes worthless. What you have in gold or canned goods or real estate, that will be your assets – hard assets.”

David McAlvany, President of the McAlvany Financial Companies, talks about the Fed’s policies and if they may be heading toward a Zero Interest Rate Policy.

A strong headline GDP release last Friday may bode well for silver demand, said Will Rhind, CEO of GraniteShares.

Rhind said that one reason silver has not performed well is due to China’s lower than expected demand, but with GDP numbers showing strength in the U.S. economy, this trend may reverse course.

“Part of the reason why silver hadn’t really been doing much is that we expected China to ease and that would be positive for the silver market in terms of stimulating demand, but of course that has slightly changed a little bit with China [focusing] more on reforms rather than outright easing,” Rhind told Kitco News.