There is also, of course, a welter of news coverage of the increasing hostilities between China and the U.S. over trade and technology. Does it therefore follow that the trade war is to blame for the turbulence in markets? We should not take this for granted.

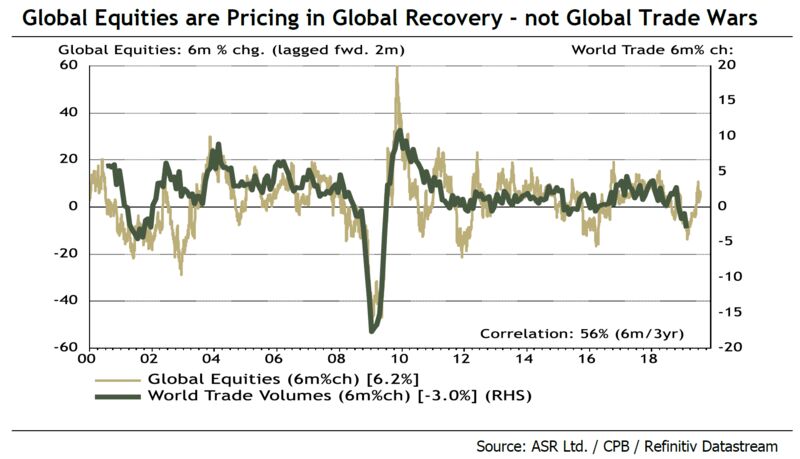

So, could this be about world trade? Equity traders do not generally think of world trade data much in their day-to-day work, but it turns out that changes in equities do tend to predict changes in global trade volumes. The following chart, from London’s Absolute Strategy Research, shows that equity market moves tend to move ahead of changes in trade flows, with a six-month lag:

The issue here is that the rebound in world equities since the Christmas Eve selloff suggests that traders are pricing in a trade recovery. This would imply that they are due quite a correction. Further, trade volumes appear to be enduring the most significant interruption yet to their steady improvement since the aftermath of Lehman’s bankruptcy:

A further argument that this market selloff, unlike the one that preceded it in December, is about trade, might come from the relative performance of emerging markets. Rightly or wrongly, they are seen as far more exposed to trade conflict than the U.S. This might explain why the sell-off at the end of last year functioned as a correction to drawn-out U.S. outperformance, while this latest moment has seen emerging markets lag behind the S&P 500 even more. At this point, all the outperformance by emerging markets since 2003 has been canceled out – an extraordinary statistic given the speed of growth in much of the emerging world.

But despite this, it is hard to say that what’s going on is just about trade. Or at least, if the trade conflict is driving this it is leading to a startling and swift reappraisal of the prospects for the economy.

The recent rise in the price of oil has gone into a sudden reverse, for reasons that can mostly be explained with reference to demand and supply (or an excess of it) in the oil market. That is an important driving factor in its own right, and tends to reduce inflation forecasts in the bond market. That said, the way breakeven rate on Treasuries have dropped in the last few weeks is startling and goes far beyond a normal reaction to a drop in oil prices:

Bear in mind also that tariffs are directly inflationary. All else equal, they increase the prices that Americans have to pay for imported goods. So this move lower in inflation expectations needs more than the trade conflict to explain it.

Meanwhile, Wednesday’s release of the minutes to the Federal Reserve’s last meeting on monetary policy suggested that the central bank was more hawkish than had been thought. In other words, the Fed is keener to keep rates higher for longer than anticipated. The response in the federal funds futures market has been to move the odds of a rate cut this year above 80% for the first time...

- Source, Bloomberg, read more here